Tax law topics

Changes to German tax law and what is planned

May 2026

Federal Fiscal Court ruling on the retroactive application of inheritance tax law

At the end of March 2026, the Federal Fiscal Court (BFH) upheld a ruling from November 20, 2025, regarding the admissibility of the retroactive application of a new legal provision as constitutionally permissible, even for gifts made before the law’s enactment.

What was the case about? In July 2016, the plaintiff transferred her share in a limited partnership (KG) as a gift. At that time, the old inheritance tax law was still formally in effect, which the Federal Constitutional Court (BVerfG) had declared unconstitutional and granted a transitional period to allow the legislature to create a new, lawful legal provision. Shortly after the gift transfer, the legislature passed a new inheritance tax law, retroactive to July 1, 2016. The tax office applied the new law, which was in effect after July 1, 2016, but before the new inheritance tax law was enacted. During the legislative process, the Federal Council (Bundesrat) invoked the Mediation Committee, which delayed the passage and entry into force of the legislation. The plaintiff sought to apply the old, more favorable law. She argued that retroactive application of the new regulations was unconstitutional because she had legitimate expectations regarding the old rules.

The Federal Fiscal Court (BFH) dismissed the appeal, ruling that retroactive application was permissible because no legitimate expectation of continued application existed, as the new regulations applied to a matter that had already been concluded. The Bundestag’s resolution of June 24, 2016, made it clear that the law would change, as mandated by the Federal Constitutional Court (BVerfG). The Federal Council’s invocation of the Mediation Committee did not alter this fact.

Therefore, following a corresponding ruling by the Federal Constitutional Court and with the legislative process at a considerable stage, taxpayers can no longer rely on the application of the old law, which has not yet been amended to their advantage.

The Federal Fiscal Court (BVerfG) has thus ruled that taxpayers can no longer rely on the application of the old law, which has not yet been amended to their advantage.

The Federal Fiscal Court (BVerfG) has already made this clear. This is of particular interest because a ruling from the Federal Constitutional Court on the current inheritance tax law is expected. If the court again declares certain provisions unconstitutional, taxpayers will no longer be able to invoke them if the legislature is already in the process of implementing the required amendments.

Those affected should seek tax advice to clarify whether and to what extent they might be affected.

Pension reform passed

The German Bundestag and Bundesrat passed the Pension Reform Act at the end of March 2026. The private pension reform is scheduled to come into effect on January 1, 2027. This will replace the so-called Riester pension scheme. Existing contracts can continue to be funded and subsidies claimed. New contracts will no longer be accepted, nor will there be automatic termination or conversion. Voluntary switching is possible.

The fundamental system of tax incentives through subsidies and the special expense deduction of savings contributions up to certain amounts will remain in place. Taxation will occur later, during the payout phase. This has the advantage that income is often lower during the payout phase in retirement, and therefore, presumably, tax rates are also lower.

The additional private pension provision will be managed through a pension account and is specifically aimed at people with little or no experience in the capital markets. It offers the option of investing with greater risk in stocks, funds, and ETFs to achieve higher returns, thus making them accessible to less experienced segments of the population. However, it remains possible to purchase guaranteed products. These products, with a maximum 1% administrative fee, will be offered by private banks and financial institutions, and potentially by a newly established sovereign wealth fund.

Retirement savings contributions will be eligible for subsidies up to an annual contribution of €1,800. The basic subsidy then amounts to 50% of the annual contribution up to €360, i.e., up to €180. For additional annual savings contributions above €360 up to €1,800 per contribution year, the basic subsidy is 25%, i.e., a maximum of €360. In total, an annual government subsidy of up to €540 per contribution year is thus possible. The maximum annual contribution is €6,840.

Parents of children for whom they receive child benefits can receive a child allowance of 100% on savings contributions up to €300 per year, i.e., an additional allowance of €300. Those who begin contributing before the age of 25 will receive an additional government subsidy of €200.

More flexible payout options will be available, ranging from a retirement plan to a payout plan that must be calculated to extend to at least age 85. Switching between different payout models will be possible. Payouts will generally begin between the ages of 65 and 70.

The group of those directly eligible now also includes self-employed individuals and mandatory members of professional pension schemes who are employed. Those in marginal employment (minijobs) who have opted out of mandatory pension insurance are excluded, as are homemakers. However, they can receive subsidies as indirectly eligible beneficiaries if they are married to or in a registered civil partnership with a directly eligible person.

Deadline: Implementation of the Pay Transparency Directive

The November 2025 issue of this publication reported on the content and implications of the European Pay Transparency Directive, which was to be transposed into national law by June 7, 2026. This directive has a particular impact on the operations of human resources departments in companies. The directive aims to reduce gender pay gaps and ensure equal pay for equal work or work of equal value.

To date, no draft bill has been published. An expert commission submitted its report in October 2025 and proposed integrating the European Pay Transparency Directive into the existing national Pay Transparency Act. The commission recommended implementing the right of employees to information about their individual remuneration as well as the average remuneration of comparable employee groups, broken down by gender.

Furthermore, salary ranges and collective bargaining agreements should be clearly stated during the application process. Questions about previous salaries should be prohibited during the application process. The expert commission recommends clear guidelines for reporting obligations and accompanying support to ensure practical implementation.

If there is no national implementation of the EU Directive by June 7, 2026, public sector employees can directly derive their rights from it. While they cannot directly invoke the provisions of the European Pay Transparency Directive in private companies, they have a right to a directive-compliant interpretation of the EU Directive from employers and courts.

The Anti-Discrimination Agency’s website offers a guide to equal pay and all assessment tools (www.antidiskriminierungsstelle.de – About Discrimination – Areas of Life – Working Life – EC Check).

Important: Since the legislative process typically takes several months, employers should expect at least a transition period without implementation and prepare immediately for adaptation to the EU Directive, as well as aligning their internal processes with the directive.

April 2026

The Federal Ministry of Finance publishes practical guidance on active pensions

Since January 1, 2026, regulations have been in effect regarding the so-called “active pension,” which provides a new tax allowance for employees subject to mandatory pension insurance who have reached the statutory retirement age (taking into account the transitional provisions) and continue working voluntarily.

An amount of up to €2,000 per month remains tax-free. This applies to both those with unlimited and limited tax liability. In 2026, the statutory retirement age is 66 years and 2 months for those born in November and December 1959, and 66 years and 4 months for those born between January and October 1960. Health insurance status is irrelevant, as is whether an old-age pension is received. Social security contributions remain unchanged.

Since many details regarding the practical implementation of the active pension scheme remained unclear, the Federal Ministry of Finance (BMF) published a question and answer catalog, which is available on the BMF website (www.bundesfinanzministerium.de – Service – FAQ and Glossary – FAQ). In addition to general information, this catalog also contains answers to specific questions for employers and employees in separate sections.

The decisive factor for claiming the tax-free allowance is the current occupation. A retired civil servant can receive it after reaching the standard retirement age if they take up employment subject to pension insurance contributions, as can a formerly self-employed person. There is no entitlement to the tax exemption for early retirement at age 63. However, if the social security system classifies an activity as subject to pension insurance contributions, the allowance can only be claimed if it is considered employment for tax purposes, e.g., for freelance teachers.

The tax-free allowance is a monthly amount, not an annual amount. It can only be claimed for months in which the requirements for the active pension are met. Special payments can, however, be divided into a pro-rata monthly payment, although this does not increase the maximum tax-free amount. The employer takes the tax-free allowance into account in the payroll tax deduction process and shows the amount as tax-free in the monthly payslip up to a maximum of €2,000 gross. Accordingly, an entry labeled “Tax-free allowance for active pension” (without spaces) must be made in a blank line of the annual wage tax statement. The active pension is not considered in the calculation of wage tax and thus in the calculation of the lump-sum allowance for social security contributions. If the employee has multiple jobs, the tax exemption may only be granted for the first job; the second job must be taken into account in the income tax return. If the employee is paid according to tax class VI, they must provide confirmation that the active pension is not being paid concurrently in another job.

Severance payments are not considered when calculating the tax-free allowance for active pensions, as they are exempt from social security contributions regardless of whether they exceed the allowance amount. However, the payment of social security contributions is a prerequisite for receiving an active pension. Employees in so-called “midi-jobs” (low-wage jobs) with reduced social security contributions can benefit from the tax exemption of active pensions.

Other tax-free income does not reduce the tax-free allowance for active pensions. Business expenses are not considered; however, they may need to be divided into a deductible and a non-deductible portion. The same applies to pension contributions.

Federal Fiscal Court: New rulings on real estate transfer tax

On October 22, 2025, the Federal Fiscal Court (BFH) issued two rulings concerning real estate transfer tax. In one case, the BFH ruled that the tax base for real estate transfer tax is not solely the purchase price of a property, but that the capitalized annual value of a personal right of residence increases the tax base. In the present case, the right of residence had not yet come into existence because it was not yet registered in the land register; however, the buyer had already consented to its transfer and thus assumed an obligation with a monetary value.

In another case, the BFH ruled, based on the same reasoning, that even an unregistered usufruct right increases the tax base if the obligation has already been assumed. This value, too, must be capitalized. In the case at hand, a leasehold was transferred for consideration and augmented by the obligation to grant a usufruct right.

New BMF letter on building modernization

Expenditures for maintenance and modernization measures on buildings are generally considered maintenance expenses and are immediately deductible as business expenses or advertising costs. However, if they are acquisition or production costs, or acquisition-related production costs, they can only be taken into account to reduce taxes over the years through depreciation.

In particular, if more than 15% of the building’s acquisition or production costs are spent on modernization measures or extensions within the first three years after acquisition, these are generally considered acquisition-related production costs, which are not immediately deductible.

Details were previously provided in an administrative letter from the Federal Ministry of Finance (BMF) from 2003 and another from 2017, which have now been superseded by a new letter dated January 26, 2026, and are applicable to all open cases.

In particular, if more than 15% of the building’s acquisition or production costs are spent on modernization measures or extensions within the first three years after acquisition, these are generally considered acquisition-related production costs, which are not immediately deductible. A key focus of the Federal Ministry of Finance’s (BMF) letter is the precise description of various building standards, as the choice of a specific building standard constitutes a determination of purpose. Extensive design options exist within the framework of building modernization, the tax treatment of which is complex. When planning extensive modernization measures, tax advice should be sought before implementation.

Double household management: Motorhome as a second household and parking space costs as rental costs?

The Federal Fiscal Court (BFH) once again had to make a decision regarding the maintenance of two households. The case concerned whether parking space costs for a vehicle used by the taxpayer at their second residence in Germany could be considered deductible business expenses. Generally, these costs are limited to €1,000 per month for domestic use. The tax authorities rejected the separate deduction for the parking space, but the lower tax court and the BFH allowed it, even though the €1,000 per month limit had already been exceeded.

The rental agreement for the parking space, with a separately stated rent, was linked to the apartment lease. However, this was irrelevant to the courts, as the two uses—residential and parking—were distinct. It was purely coincidental that the landlord of the apartment was also the landlord of the parking space. Contrary to the Federal Ministry of Finance’s letter of November 25, 2020, there are explicitly two separate contracts and uses.

In another case, the Baden-Württemberg Tax Court (FG) had to decide whether the use of a motorhome at the domestic place of work, instead of a permanent residence, qualifies as a deductible double household. The taxpayer used this motorhome to travel to his primary residence on weekends and then back to his place of work. The plaintiff sought, among other things, to have the depreciation of the motorhome recognized as business expenses. The tax authorities rejected this claim, arguing that it did not constitute independent accommodation suitable and intended for permanent residence.

The Tax Court considered a motorhome generally suitable for living at the primary place of work. However, the court ruled that the second residence must be physically separated from the primary residence for a considerable period of time. This requirement was not met because the taxpayer also used the motorhome for trips home. Had the taxpayer left the motorhome at his primary place of work, it would have been recognized as a second residence. Nevertheless, the Tax Court did allow the taxpayer to deduct travel expenses for these trips home. The appeal to the Federal Fiscal Court was not admitted, and the complaint against the refusal of admission was rejected.

Base interest rate for the advance lump sum for investment funds announced

At the beginning of the year, the advance lump-sum tax is deducted from the clearing account of investment funds, unless a tax exemption order of sufficient amount is in place.

The advance lump-sum tax serves to ensure the taxation of income from investment funds, even if this income is not (yet) distributed to investors. To guarantee the timely taxation of this theoretical income, the tax office collects the tax as an advance payment instead of waiting until the fund units are sold. In that case, a settlement takes place later upon sale.

Part of the calculation of this advance lump-sum tax is the base interest rate set by the Federal Ministry of Finance, which has been set at 2.53% for 2025. This applies to the advance lump sum tax for 2025, calculated on the first working day of 2026.

For the calendar year 2026, the base interest rate was set at 3.2% by the Federal Ministry of Finance (BMF) letter of January 13, 2026. The advance lump sum tax for 2026 will then be calculated from this rate at the beginning of 2027.

Investors who have not submitted an exemption order for their securities account should consider doing so or ensure they have sufficient funds available in their settlement account at the relevant time for tax collection in January of each year.

auto_awesome Did you mean: EuGH: Wann Fahrzeit als Arbeitszeit gilt 41 ECJ: When travel time counts as working time

The European Court of Justice (ECJ) recently had to decide, based on the European Working Time Directive, when travel time counts as working time for employees without a fixed place of work. The German Federal Labour Court (BAG) had already addressed this issue in 2020 in the case of service technicians. The question is also particularly relevant for construction site and field service employees.

In the initial case, a Spanish company had its employees meet at a depot, from where they traveled together at a fixed time in a company vehicle to the work sites designated monthly by the employer. The vehicle was driven by an employee and also transported the necessary materials. The employer recognized the journey to the work site as working time, but not the return journey, during which the employees were dropped off at the meeting point and drove home independently. The EU Working Time Directive recognizes only working time or rest time, not an intermediate form.

Since employees do not perform any work during journeys, have no free disposal of their time or activities, and the travel arrangements are determined by the employer, the European Court of Justice (ECJ) has ruled that both journeys count as working time for the driver and passengers. The ECJ thus focuses primarily on the employer’s organizational structure, rather than, as previously held by the German Federal Labour Court (BAG), on the level of workload, e.g., in comparison to the driver and passenger.

This has implications for working time law. Travel time must be taken into account when calculating maximum daily working hours, rest periods, occupational safety, and time recording. The employer’s obligation to compensate for travel time is regulated by the respective national law; in Germany, this is governed by labor law, contract law, and collective bargaining law. According to previous BAG case law, an obligation to compensate arises if the journey takes place during working hours, is carried out at the employer’s instruction, or is in the employer’s interest. A separate compensation agreement can be made.

March 2026

Federal Fiscal Court (BFH): Parking space costs for company cars do not constitute a reduction in benefits

The Federal Fiscal Court (BFH) ruled on September 9, 2025, that costs borne by an employee for a parking space or garage do not reduce the taxable benefit arising from the provision of a company car for private use.

In the case at hand, the employer had factored in the employee’s payment of €30 per month for the use of a parking space as a deduction when calculating the taxable benefit for private use in the payroll calculation, thus reducing the taxable benefit. It was calculated according to the 1% rule.

Following a payroll tax audit by the tax office, the office demanded additional payroll tax for the parking space. The objection proceedings were unsuccessful. The employer appealed to the Tax Court. In the first instance, the Cologne Tax Court ruled in favor of the employer.

However, in the appeal proceedings, the Federal Fiscal Court overturned the first-instance ruling. The Federal Fiscal Court (BFH) holds that the provision of a parking space or garage generally constitutes a separate benefit in kind, distinct from the benefit of being provided with a company car. Parking space costs are therefore not included in the total vehicle costs covered by the 1% rule or the logbook method.

It follows that an employee’s payment for a parking space can only reduce the benefit derived from the provision of the parking space. For example, if the employee pays only €30 for parking, even though €50 per month would be appropriate, the payment cannot reduce the benefit derived from the private use of the company car. Only expenses that are part of the benefit derived from the private use of the company car, such as fuel, insurance premiums, and maintenance costs, can reduce the benefit. Costs that are not directly related to the use, maintenance, or operation of the vehicle, or that depend solely on the employee’s decision, cannot be considered as reducing the benefit. In this respect, parking space costs are treated the same as costs for using a ferry or tolls. Seek legal and tax advice when drafting employment contracts and company car policies.

Electric car subsidy program retroactive to 1 January 2026

Starting in May 2026, private households will be able to apply retroactively for subsidies for the purchase or lease of newly registered, all-electric cars, as well as certain plug-in hybrids and range extenders, via an online portal, regardless of the list price. These subsidies are valid for the period from January 1, 2026. A total of €3 billion is available for the years 2026–2029. Eligible vehicles must be kept for at least three years.

The subsidy for all-electric vehicles ranges from €3,000 to €6,000, depending on the household’s taxable annual income and the number of children under 18. The highest subsidy is available for households with two or more children and a taxable annual income of up to €45,000, while childless households with an income exceeding €80,000 are not eligible for any subsidies.

The subsidy for all-electric vehicles ranges from €3,000 to €6,000, depending on the household’s taxable annual income and the number of children under 18. When purchasing an eligible plug-in hybrid or electric vehicle with a range extender, the subsidies are lower, ranging from €1,500 to €4,500 depending on household income and the number of children. For these vehicles, CO2 emissions must not exceed 60 g/km, or the electric driving range must be at least 80 km. The subsidies for these vehicles will be reviewed again on July 1, 2027.

A FAQ on electric vehicle subsidies can be found on the website of the Federal Ministry for the Environment under the heading “Subsidies.”

Apply for property tax relief in case of loss of income until March 31, 2026.

Owners of properties or apartments that experienced vacancy, loss of rental income, or force majeure (e.g., official prohibition of use, fire/water damage) in 2025 through no fault of their own can apply for a waiver or partial waiver of property tax by submitting an informal application. Depending on the extent of the loss, the waiver can range from 25% to 100% in the case of total loss. It is irrelevant whether the property is residential or commercial.

The application must be submitted by March 31, 2026, at the latest. This deadline cannot be extended. Generally, the city or municipal administration is responsible; in the city-states of Hamburg, Berlin, and Bremen, the tax office is responsible.

Grace period until mid-March 2026: Disclosure of the 2024 annual financial statements

The deadline for disclosing financial statements for the fiscal year ending December 31, 2024, was December 31, 2025. The Federal Ministry of Justice has announced that proceedings for administrative fines due to the late disclosure of annual financial statements will not be initiated until mid-March 2026. Until then, it is still possible to disclose the financial statements, albeit late, without incurring a fine. This is a final extension of the deadline. The deadline for filing tax returns is April 30, 2026.

Maintenance payments only reduce taxes if made by bank transfer.

Maintenance payments, for example from parents to their children, can be recognized as extraordinary expenses for income tax purposes under certain conditions. A prerequisite is that there is a legal obligation to provide maintenance to the recipient and that the recipient is not entitled to child benefit or a child tax allowance. If the person receiving maintenance lives in Germany, their tax identification number must be provided. The recipient must have only minimal assets.

The tax deduction is limited to the basic tax allowance plus any contributions to health and long-term care insurance. This allowance is €12,096 for 2025 and €12,348 for 2026. However, this basic tax allowance is reduced by any income and benefits of the recipient that exceed €624 annually.

The Federal Ministry of Finance (BMF) issued two letters dated October 15, 2025, stating that maintenance payments made domestically and internationally from the 2025 tax year onward can only be recognized as extraordinary expenses if the payment is made by bank transfer to the recipient’s account, provided all other requirements are met.

The taxpayer is responsible for ensuring that easily verifiable documentation exists proving that the funds used originate from the taxpayer and have been transferred to the recipient.

Further requirements for situations involving foreign recipients are detailed in the corresponding BMF letter.

Transfers to an account not held in the recipient’s name generally do not meet the requirements for tax deductibility. Exceptions may be granted in cases involving typical maintenance expenses such as… For example, rent payments for an apartment can be made directly to the third party’s account in the name of the recipient of maintenance payments to fulfill the rent payment obligation.

Further requirements are detailed in the German Federal Ministry of Finance’s (BMF) circular for domestic transactions.

49 Lump sums for non-cash benefits 2026

The Federal Ministry of Finance (BMF) announced the flat-rate amounts for non-cash withdrawals (non-cash transfers) of food and beverages applicable for the 2026 calendar year in a letter dated December 23, 2025. These amounts have been slightly increased. They are net annual amounts. For monthly entries, the amounts must be prorated by twelve.

The legislator assumes that individuals who sell food and beverages commercially also consume them privately. Normally, individual records of the withdrawn value must be kept for private consumption. This effort is generally only worthwhile for low levels of personal consumption.

For simplification purposes, the legislator has therefore introduced flat-rate amounts for non-cash withdrawals, which vary depending on the business sector. Anyone operating a restaurant (of any kind), café, bakery, confectionery, butcher shop, retail food or beverage store, fruit or vegetable shop, or dairy or egg retail business can find the applicable standard values for goods withdrawn from the premises in the list published by the Federal Ministry of Finance (www.bundesfinanzministerium.de – Topics – Taxes – Tax Administration & Tax Law – Tax Audit – Guideline Collection / Flat-Rate Amounts). Individual records are not required when using these standard values.

It is important to note that, for example, a bakery owner is not classified as a food retailer if they also have a refrigerator in the sales area from which, for example, milk, cheese, and eggs are sold, and the revenue from this is of minor importance. Only one standard amount is to be applied, in this case, the higher of the two.

These amounts range from €399 per adult per year (excluding VAT for beverage retailers) to €4,001 (for restaurants serving hot and cold food), depending on the type of business. For the latter, the amount was reduced due to the reduction of the VAT on food from 19% to 7%. Children under 2 years of age are not included; children aged 2–12 years are included at half the annual flat rate.

Withdrawals that are not food or beverages, such as tobacco, magazines, clothing, or electronics, must always be recorded individually and entered into the accounting records.

February 2026

North Rhine-Westphalia purchases data carriers for the detection of tax evasion

Tax authorities are increasingly cracking down on tax evasion and investigating suspected cases. In addition to combating undeclared work and conducting customs inspections, recent investigations have focused on large-scale investigations targeting cryptocurrency traders and investors, landlords of accommodations listed on Airbnb, and social media influencers on suspicion of tax evasion. Tax justice is a hot topic, public coffers need revenue, and government agencies are catching up in investigative work by utilizing digital technology.

The latest “catch”: In December 2025, the State Office for Combating Financial Crime in North Rhine-Westphalia announced that it had purchased a 1-terabyte data storage device from a whistleblower containing incriminating material, which is said to contain highly valuable information for uncovering large-scale tax evasion.

Specifically, the data is believed to include customer information from service providers with business locations in the United Arab Emirates, the Cayman Islands, Hong Kong, Mauritius, Panama, Singapore, and Cyprus. These service companies offer assistance in setting up foreign companies in low-tax jurisdictions with the aim of concealing taxable funds from the German tax authorities or obscuring the true ownership structures through shell companies and shareholder structures.

The State Office has reviewed the data and identified individuals residing in Germany and other countries. This data is currently being processed and will also be made available to other authorities abroad. The Federal Ministry of Finance, the Federal Government, and the other German states were informed of the data purchase on December 11, 2025. No information is yet available regarding the amount of money that flowed into the overseas companies.

Investors should check whether they have knowingly or unknowingly invested assets as described and gather the relevant documentation. They should contact a tax advisor as soon as possible, especially if they are not yet aware of any investigation being initiated by the tax authorities.

Tax advisors can prepare corresponding supplementary declarations and, depending on the stage of the proceedings, advise on the right time for a self-disclosure that is still possible or no longer possible to avoid prosecution.

Permanent VAT reduction to 7% from 1 January 2026 for food in the catering industry, restaurants & catering services

Until December 31, 2025, restaurants and other food service establishments were required to charge a flat rate of 19% VAT on food and beverages intended for on-site consumption, and a reduced rate of 7% for takeaway and delivery food. A temporary VAT reduction for food was in effect during the COVID-19 pandemic. With the 2025 Tax Amendment Act, the legislature has permanently reduced the VAT rate to 7% for food in restaurants, catering services, and similar businesses, effective January 1, 2026. For the night of December 31, 2025, to January 1, 2026, businesses have the option to choose between the two rates. The standard VAT rate remains in effect for beverages.

The distinction between prepared food for on-site consumption, takeaway, or delivery has been eliminated. The reduced VAT rate applies uniformly. Businesses must adjust their point-of-sale and accounting systems to ensure the correct tax rate is displayed from January 1, 2026. Menus, invoices, tax information on vouchers, and VAT returns must be updated accordingly. Combination offers must be checked for correct allocation; if necessary, the beverage portion can be taxed at a flat rate of 30%. Any incorrect or excessively high tax shown on receipts and invoices must be reported to the tax office. If you have any questions, consult a tax advisor beforehand.

Input tax deduction when transitioning from small business to standard taxation

Effective January 1, 2025, the German legislature has revised the taxation of small businesses, aligning it with EU law. As a result, taxpayers currently using the small business scheme may be required to switch to standard taxation if their revenue exceeds the threshold in the current calendar year. The Federal Ministry of Finance (BMF) issued a statement on November 10, 2025, addressing the specific aspects of input tax deduction and its application.

Small businesses based in Germany that do not exceed €100,000 in annual revenue in the current calendar year and did not exceed €25,000 in the previous year can have their revenue exempt from VAT. This means they do not pay VAT, cannot charge it, and are also not entitled to claim input tax credits when receiving invoices from other businesses.

Those switching from small business status to standard taxation are generally entitled to input tax credits from that point onward. For invoices received when the company was still a small business, the German Federal Ministry of Finance (BMF) considers it crucial whether the services shown on the invoice are used for sales subject to standard taxation only after the change in taxation status. Conversely, a change from standard taxation to the small business scheme may result in a reclaim of input tax from the tax office.

In both cases, the input tax must generally be adjusted. In practice, this will typically affect assets in the upper price segment, as input tax deduction adjustments only occur above €1,000 if they pertain to the acquisition or production costs of an asset, such as machinery or vehicles.

The BMF letter applies to open cases. If the VAT return was submitted by November 10, 2025, the old regulations may be applied as an alternative.

Subsequent reduction of the monthly pension in Riester contracts

A case decided by the German Federal Court of Justice (BGH) concerned unit-linked Riester pension insurance policies, where the future pension amount is calculated based on a pension factor specified in the policy. This pension factor is based on the insurer’s assumed actuarial assumptions, in particular the guaranteed interest rate and the calculated life expectancy, and determines the monthly pension for every €10,000 of policy value.

The general terms and conditions of insurance used in some contracts stipulated that the insurer could reduce the pension factor if unforeseen circumstances arose after the conclusion of the contract, such as a significantly increasing life expectancy or permanently declining capital market returns. Based on this clause, the insurer had repeatedly lowered the pension factor.

The BGH declared this clause invalid. While an insurer can react to subsequent disruptions in the economic equilibrium in long-term pension contracts, a unilaterally structured right of adjustment is deemed unreasonable. The clause permitted only a reduction in the pension benefit but did not obligate the insurer to increase the pension factor again if circumstances subsequently improved.

This provision therefore violates the principle of symmetry. This principle requires that deteriorations and improvements in the relevant circumstances be treated equally. An insurer who reserves the right to reduce benefits must therefore also be obligated to pass on positive developments to policyholders in a comparable manner.

Statutory minimum wage – not fulfilled by company car

The statutory minimum wage cannot be fulfilled by providing a company car. The Minimum Wage Act requires a monetary payment. A company car cannot be used to fulfill the minimum wage obligation.

Therefore, in addition to the social security contributions already paid for providing a company car, an employer must also pay contributions towards the statutory minimum wage, as providing a company car does not fulfill the minimum wage requirement. Social security contributions become due upon its accrual, as stipulated by law. These are not covered by the contributions already paid for providing the company car.

As the Federal Labor Court ruled in 2016, the statutory minimum wage requirement is only fulfilled when the gross remuneration paid for the calendar month reaches the amount calculated by multiplying the number of hours actually worked in that month by the statutory minimum wage.

Overtime pay for part-time employees

The Berlin-Brandenburg Regional Labor Court has ruled that a collective bargaining agreement stipulating that all employees, including part-time workers, only receive overtime pay after exceeding the weekly working hours for full-time employees constitutes legally prohibited discrimination against part-time workers. The legal consequence is a court-ordered upward adjustment, meaning that even for part-time employees, exceeding their individual weekly working hours triggers the collectively agreed overtime pay obligation.

This decision was based on the following facts: In the collective bargaining agreement for retail employees in the state of Brandenburg (MTV), the contracting parties stipulated an overtime pay supplement of 25% for exceeding the collectively agreed weekly working hours for full-time employees, which are generally 38 hours. An employee worked part-time in sales. Over a six-month period, she worked 62 hours in excess of her contractually agreed weekly working hours, but never more than 38 hours in any single week. In her lawsuit, she argued that she was being discriminated against as a part-time employee compared to full-time employees and was entitled to overtime pay for 62 hours. The employer refused, citing the collective bargaining agreement and the constitutional protection of collective bargaining autonomy.

The Federal Labor Court also ruled on November 26, 2025, that part-time employees are entitled to the collectively agreed overtime pay if they exceed their individual weekly working hours proportionally to the overtime pay threshold for full-time employees.

January 2026

January 2026

Workation: What employers and employees need to know

When companies based in Germany allow their employees to work remotely from abroad on short notice, also known as workation, this is one of several criteria for many job seekers when deciding whether or not to accept a position with that company or to change jobs. According to a workation study, well over half of all employees now expect their employers to offer remote work options not only within Germany but also from abroad.

However, both companies and employees are often insufficiently informed about the legal and tax requirements and consequences. Employment contracts and supplementary agreements frequently lack legally sound provisions.

Clearly defined regulations are crucial, not least for liability reasons. Companies should therefore review, or have reviewed, the relevant tax, labor, and social security regulations beforehand. Workation must be clearly distinguished from a permanent assignment abroad for the company, and working in a foreign branch of a German company does not constitute workation.

The following points should be clarified or contractually agreed upon in advance:

Internal company regulations should clarify which employee groups can take advantage of the workation offer.

For a temporary workation of up to four weeks, German labor law applies, and public holidays at the place of work also apply to the employee.

For a workation lasting longer than four weeks, the company must provide the employee with written confirmation of this, as well as further information, such as the duration of the stay and the currency in which the remuneration is paid (Proof of Employment Act).

For a workation lasting more than six months, the labor law of the host country applies with regard to remuneration, notice periods, working hours, and vacation entitlements.

Longer workations in non-EU countries generally require a visa; a tourist visa is not sufficient. A work visa or a special workation visa may be required, which is already available in some countries.

Caution: Anyone working without a work permit is considered illegally employed and may be deported and banned from re-entering the country. For the employer, such actions can lead to a business closure order and substantial fines.

Within the EU, the EEA, and Switzerland, employees can stay for work purposes without restrictions. A visa is not required. However, reporting or registration requirements must be observed in most countries.

Those who work abroad for a maximum of 183 days per year remain subject to unlimited tax liability in Germany; for longer stays, tax liability arises in the foreign country.

If a workation lasts longer than four weeks, the employer, in particular, must be aware of the labor and tax law implications. Employers should always inform themselves about these matters independently.

Compliance with social security requirements and consequences is also important.

For a workation in a third country – outside the EU – it must be checked whether a social security agreement exists between Germany and the respective country. This information should be obtained well in advance. Consultation with a specialist in international assignments is helpful in this regard.

For a workation within the EU, EEA, or Switzerland, the employee needs an A1 certificate, which serves as proof of insurance coverage and can be applied for electronically by the employer or employee.

It should be noted that since 2025, cross-border commuters also require such an A1 certificate, even if no workation takes place.

If an employer approves a workation in another EU country, this is considered a posting for social security purposes. The employer is then liable for ensuring that their employees and accompanying family members have health insurance coverage.

The temporary posting of an employee from Germany to another European country on behalf of the domestic company must be limited in time in advance. The remuneration must be accounted for in Germany. An international assignment does not exist if the seconded person lives abroad and is hired by a German company to work in their home country or another country. The person must not have been employed in Germany prior to this assignment or have previously had their residence or habitual abode in Germany.

January 2026

Companies that do not wish to submit their monthly VAT returns by the 10th of the following month or make VAT prepayments by the 13th of the following month can apply for a so-called permanent extension of the filing deadline for the year 2026 by February 10, 2026. A special VAT prepayment amounting to one-eleventh of the previous year’s VAT liability must be paid to the tax office. The VAT returns and/or payments may be submitted or made one month later. Companies that file quarterly are not required to make special prepayments. The amount of the respective special VAT prepayment can be accessed via ELSTER from January 1, 2026. The special prepayment will be offset against the VAT prepayment for December.

Note: Since October 9, 2025, banks have been required to verify the recipient’s name against the IBAN to prevent erroneous online transfers and fraud. If the recipient’s name and IBAN do not match, the transfer will initially not be processed. The customer will be notified of a different account holder and can select the correct one. Once the customer confirms the transfer, the bank is no longer liable for any erroneous transfers. This also applies to real-time transfers. This rule does not apply to paper-based transfers.Tax assessments do not always include the recipient’s details, but sometimes only the IBAN. Therefore, it is essential to verify the account details in a timely manner to avoid missing payment deadlines.

January 2026

Gift: Contribution of the family home to a GbR (general partnership)

The Federal Fiscal Court (BFH) had to decide whether the contribution of a family home by a sole-owning spouse to a general partnership (GbR) in which both spouses each hold a 50% share, triggers the assessment of gift tax against the other spouse, the recipient. The notarized agreement described the contribution as a gratuitous, spousal gift from the wife to the husband, the plaintiff. Both spouses were registered in the land register as partners and owners of the property.

The tax office (FA) had assessed gift tax against the plaintiff as the beneficiary, even though it was undisputed that the property was a family home. The requirements for a property to qualify as a family home include, among other things, that the residence must constitute the center of the donor’s life, be used by the donor until the gift is made, and subsequently be used by the recipient. The tax office argued that the tax exemption for family homes did not apply because the property was transferred to the general partnership. Half of the property should be attributed to the plaintiff and subject to gift tax. The objection was unsuccessful. The court of first instance upheld the appeal and amended the gift tax to €0, reasoning that the acquisition of jointly owned property is also tax-free as a family home. The Federal Fiscal Court (BFH) found the tax office’s appeal to be unfounded and dismissed it.

According to the BFH, in the case of a general partnership (GbR), the individual partner is liable for the tax, not the partnership as a whole, even though the GbR has partial legal capacity and is eligible for registration. Therefore, a developed property is also considered a family home, which constitutes the core of a couple’s life and economic community. The legislature has expressly privileged this and exempted it from taxation.

January 2026

Contribution to voluntary private long-term care insurance as a special expense

The Federal Fiscal Court (BFH), acting as the court of appeal, has ruled that, in addition to contributions to basic private health insurance, only contributions to mandatory private long-term care insurance are fully deductible as special expenses for income tax purposes. This does not apply to contributions to supplemental private long-term care insurance. These contributions are only partially deductible and often have no tax benefit for the taxpayer.

This ruling was consistent with the decisions of both the tax office in the initial assessment proceedings and the Hessian Fiscal Court in the first instance.

The plaintiffs argued that it would be unconstitutional if, in cases of long-term care needs, particularly in inpatient care, those requiring care were reduced to the status of “beggars” due to high out-of-pocket expenses. They maintained that the state must therefore at least recognize contributions to supplemental private long-term care insurance for tax purposes, thereby providing some financial relief to taxpayers.

The Federal Fiscal Court (BFH), however, takes the view that the legislature initially intended to provide only partial coverage for the population as a safeguard against the need for long-term care. After it was recognized that the pay-as-you-go long-term care insurance system had gaps, the legislature created the long-term care allowance as a supplementary, eligible form of protection, rather than private long-term care insurance. The plaintiffs, however, did not want to utilize this allowance because they considered the premiums less favorable.

According to the BFH’s decision, it is constitutionally permissible for the legislature to exempt from taxation only that portion which it deems mandatory and which is intended to protect against reliance on social assistance.

January 2026

The Federal Fiscal Court will publicly announce its decisions in three cases on December 10, 2025 (after the editorial deadline of this edition).

This is of particular interest to property owners in the federal states that have implemented the property tax reform according to the federal model. These states are Berlin, Brandenburg, Bremen, Mecklenburg-Western Pomerania, North Rhine-Westphalia, Rhineland-Palatinate, Saxony-Anhalt, Schleswig-Holstein, and Thuringia. Saarland and Saxony also use the federal regulations, with variations in the tax assessment rate.

The federal model determines the property value for residential properties based on the plot and living space, as well as the standard land value, building type, and year of construction. The three cases pending before the court have in common that the constitutionality of the standardized income approach used for property tax purposes is contested.

The standardized income approach applies to single-family and two-family homes, rental properties, and condominiums. The income approach is also partially used for inheritance and gift tax purposes; however, unlike property tax, valuations are based on actual net rents, not on standardized net rents applicable across the state. Property tax only differentiates based on building type, year of construction, and living space category, which are expressed through surcharges and discounts. For example, there is no distinction between rent levels based on urban and rural location.

The question the Federal Fiscal Court (BFH) will have to answer is whether it is compatible with the principle of equality to determine the value of a property or residential unit in numerous property tax proceedings using a grossly simplified procedural approach, such as standard land values determined by expert committees and standardized net rents.

Currently, approximately 2,000 lawsuits concerning various property tax models are pending before the BFH, with 15 such cases currently before them.

January 2026

47 Increase in the minimum wage for trainees

For trainees not covered by collective bargaining agreements, a minimum wage applies. The amount of the monthly minimum wage according to the Vocational Training Act has now been updated. Here is an overview of the minimum wages from 2022 to 2026, from January 1st to December 31st. of the respective year:

| Ausbildungsbeginn | 1. Ausbildungsjahr | 2. Ausbildungsjahr | 3. Ausbildungsjahr | 4. Ausbildungsjahr |

| 2026 | 724,00 € | 854,00 € | 977,00 € | 1.014,00 € |

| 2025 | 682,00 € | 805,00 € | 921,00 € | 955,00 € |

| 2024 | 649,00 € | 766,00 € | 876,00 € | 909,00 € |

| 2023 | 620,00 € | 731,60 € | 837,00 € | 868,00 € |

| 2022 | 585,00 € | 690,30 € | 789,75 € | 819,00 € |

December 2025

December 2025

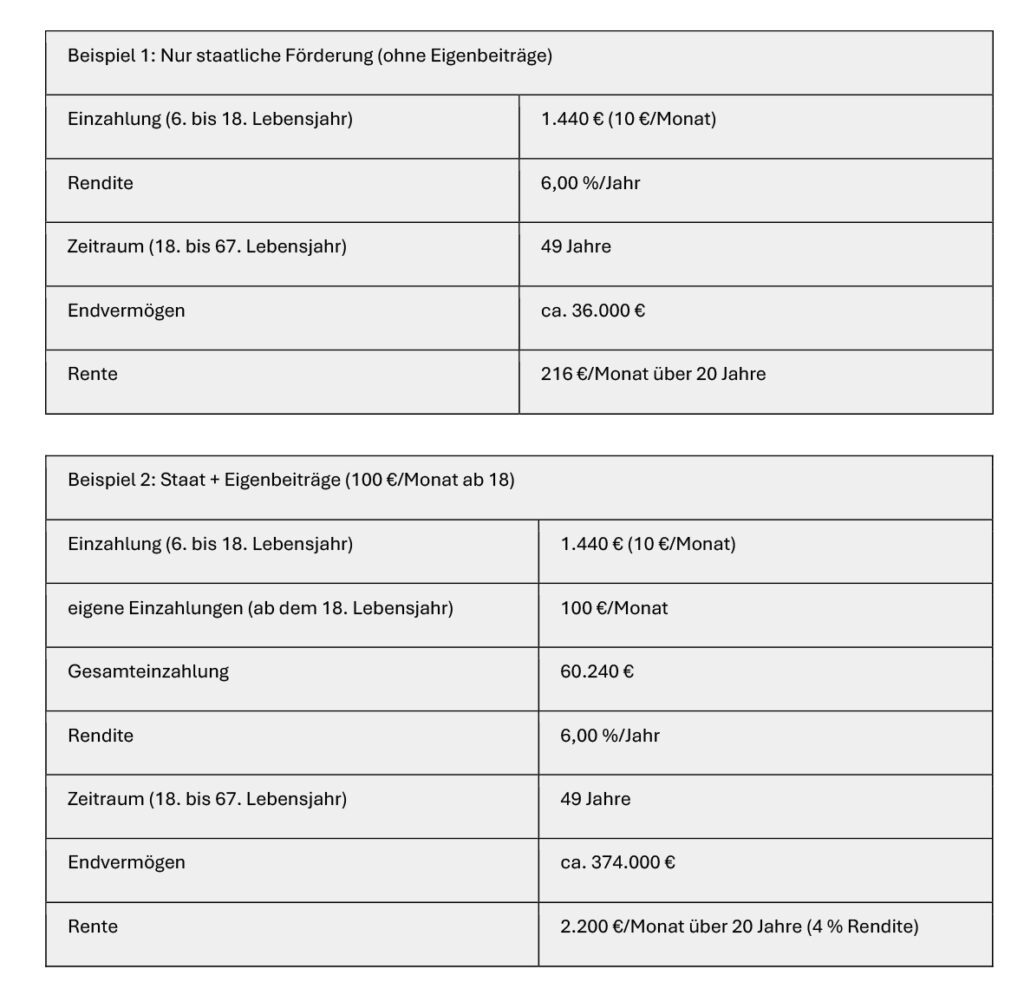

The early retirement pension

The so-called “early start pension” is to be introduced in Germany with the aim of supporting parents in their children’s early retirement savings, allowing them to benefit from compound interest. This is intended to relieve the burden on the pension system in the future. Whether it can come into effect at the beginning of 2026, as initially planned, is currently unclear, as no draft legislation or bill has yet been presented. The early start pension is to be linked to a reform of tax-advantaged private retirement savings.

Children from the age of six are apparently to receive a state-subsidized securities account without having to apply, into which €10 is paid monthly between the ages of six and eighteen. From the age of eighteen, the now-adult child can then contribute €50 to €100 per month to the account. However, there are differing proposals from the insurance industry.

Assuming a weighted average annual return of 6% and no personal contributions, Example 1 below shows a pension capital of approximately €36,000, or a monthly pension of €216 over 20 years. Example 2 assumes monthly contributions of €100 to the contract starting at age 18, resulting in a pension capital of approximately €374,000, in addition to the government subsidy, or a monthly pension of €2,200.

The contract cannot be terminated before age 67, and the capital cannot be used for other purposes. If the retirement age were to increase to, for example, 70, the pension capital in Example 1 would increase slightly due to the three-year extension, while in Example 2, it would increase more significantly due to the higher contributions. No information is currently available regarding the taxation of the returns.

The contract cannot be terminated before age 67, nor can the capital be used for other purposes. It is not yet known what inheritance law ideas the legislator has, for example, in the event of the death of the beneficiary before (fully) receiving the pension.

December 2025

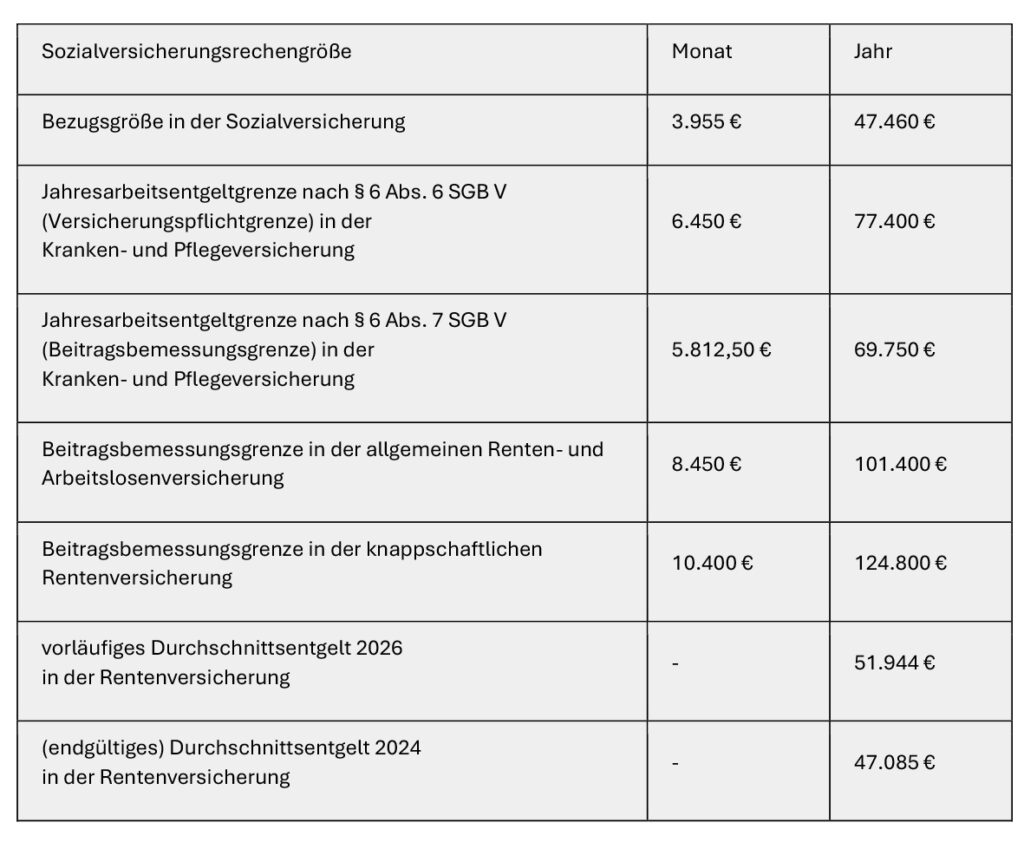

On October 8, 2025, the Federal Cabinet approved an increase of more than 5% in the contribution assessment ceilings for 2026; approval by the Federal Council is still pending. People with higher incomes will therefore have to pay contributions on a larger proportion of their income if they contribute to the statutory social security system. These contributions are as follows:

December 2025

Special depreciation: New replacement building = new construction?

The Federal Fiscal Court (BFH) published a long-awaited ruling on August 12, 2025, regarding the special depreciation allowance for new rental housing construction.

The case concerned an initial funding period for housing construction projects initiated by building permit application or notification after August 31, 2018, but before January 1, 2022. Currently, there is a second funding period for building permit applications or notifications for housing construction projects that commenced after December 31, 2022, but before October 1, 2029.

During the first funding period, the plaintiffs demolished a rented, usable single-family home after the tenants terminated their lease and moved out, due to an official order requiring the sewage pipes to be repaired. A new single-family home was subsequently built on the property, and a lease agreement was concluded with tenants. The tax office refused to recognize the special depreciation allowance claimed by the plaintiffs as business expenses, arguing that although the building was new, no additional living space had been created. Demolition and new construction took place within a period of approximately 1.5 years.

Neither the explanatory memorandum to the law nor the tax authorities addressed, either before or after the legislative process, whether the wording “new, previously non-existent dwelling created” should be interpreted as meaning that a new replacement building that does not create additional living space is also ineligible for the allowance, or whether a review of the demolished building was relevant, perhaps by comparing the living space and building type before and after demolition.

Both the Cologne Tax Court of first instance and the Federal Fiscal Court (BFH) found that the eligibility requirements for the special depreciation allowance were not met.

In its decision, the BFH essentially reasoned that replacing existing apartments with a similar new building does not constitute a “new, previously non-existent dwelling.” This could be different, however, if the demolition and new construction of an apartment are not temporally related, as in the case at hand.

The purpose of the regulation and the subsidy is to increase the amount of living space, not merely to replace existing housing. The special depreciation allowance is intended to counteract the housing shortage.

In the current second subsidy period, which was not addressed in the ruling, the term “new” apartment is now defined as one meeting the criteria of an “Efficiency House 40” with a sustainability factor.

However, the Federal Fiscal Court (BFH) has already indicated in its decision that the same parameters could apply here as well.

In this respect, if neither the tax authorities nor the legislature intervene to clarify the matter, a large number of lawsuits are likely.

Affected taxpayers should seek tax advice immediately if the responsible tax office has not recognized the special depreciation allowance.

December 2025

Germany Ticket 2026

The Germany Ticket is to remain in place from 2026 to 2030. According to an agreement between the transport ministers of the German states, the current ticket price of €58 in 2025 is to increase to €63 per month in 2026. In 2026, employers can continue to pay tax-free and social security-free subsidies for the Germany Ticket in addition to the employee’s regular salary. The subsidy is limited to the amount of the employee’s actual expenses.

December 2025

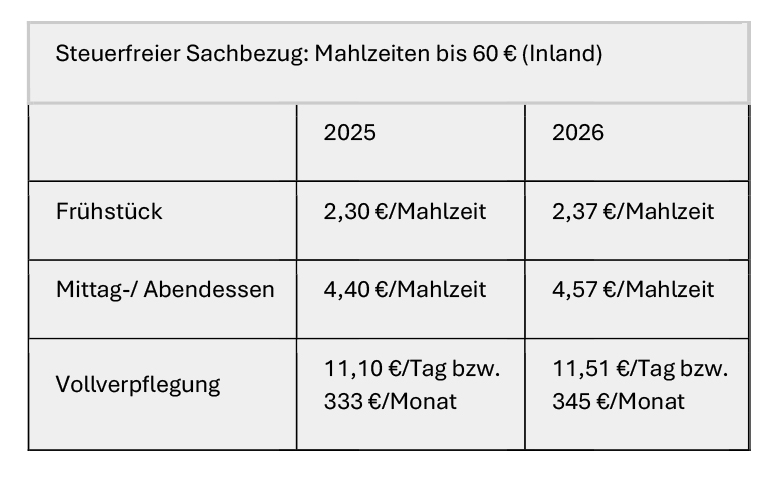

New non-cash benefit values for accommodation and meals in 2026

Free or subsidized meals provided by an employer to its employees are considered a taxable benefit in kind for the employees within the context of their employment.

According to the draft bill for the Social Security Remuneration Ordinance dated October 8, 2025, the standard values for benefits in kind are expected to increase on January 1, 2026. The amendment is scheduled to be adopted after the editorial deadline for this issue. The standard values for benefits in kind will then be as follows:

NOVEMBER 2025

November 2025

Tax Amendment Act 2025

The German Federal Cabinet has adopted the draft of the 2025 Tax Amendment Act. The Bundestag and Bundesrat are expected to approve it before the parliamentary winter recess in December so that the proposed changes can come into effect on January 1, 2026. The draft includes the following key changes:

The commuting allowance for deductible expenses related to income from employment will be increased to a uniform rate of €0.38/km, instead of the current €0.30/km, and €0.38/km for distances beyond the first 20 km.

The mobility bonus for low-income earners will be made permanent. Reimbursement will be possible for distances beyond the first 20 km, as low-income earners generally do not pay income tax from which they could deduct commuting expenses.

Tax- and social security-free expense allowances for instructors will be increased from €3,000 to €3,300 annually, and for volunteers from €840 to €960. Both allowances can be used concurrently, but from 2026 onward, they must be used to promote charitable, benevolent, or religious purposes.

For non-profit organizations, the tax-free threshold for income, including VAT, from commercial activities will increase from €45,000 to €50,000, within which no corporate or trade tax is payable. E-sports will be recognized as a non-profit activity from 2026.

The electricity tax relief for farmers and foresters will be reinstated.

The 19% VAT on food provided by restaurants and catering services will be reduced back to 7% from January 1, 2026. This also applies to catering companies, convenience stores, etc. The VAT rate for beverages will remain at 19%.

The special depreciation allowance for the construction of new rental apartments should be retained.

November 2025

The Active Pension

The so-called “active pension” is intended as one of several instruments to counteract the shortage of skilled workers. It is designed to give companies the option of employing their long-term staff beyond retirement age, if the employees in question wish to do so. Reportedly, the draft bill, dated October 9, 2025, was available to industry associations for comment until October 10, 2025, with a one-day deadline.

In addition to lifting the ban on consecutive fixed-term contracts (fixed-term employment without objective justification after a certain period of employment), the law is scheduled to come into effect on January 1, 2026, for individuals who have reached the standard retirement age. After two years, an evaluation will be conducted to determine whether the desired outcome has been achieved and to assess the cost-benefit ratio.

Pensioners will be allowed to earn up to €2,000 per month or €24,000 per year tax-free. The regulation is not intended to apply to early retirees, the self-employed, farmers, civil servants, and those in marginal employment (minijobs), so numerous legal proceedings are already anticipated due to potential violations of the principle of equal treatment and the principle of equal taxation (according to ability to pay).

According to the draft, the active pension applies only to employment relationships subject to social security contributions or income from dependent employment. Health and long-term care insurance contributions from this income are to be paid equally by the employer and employee, while pension insurance contributions are to be paid solely by the employer. The exemption from wage tax is to be applied directly through the payroll tax deduction process, not through a tax return. The wages or salary are thus to be paid directly tax-free and are not subject to the progression clause. The tax rate on other income will not be increased as a result.

An entry into force on January 1, 2026, is an ambitious goal, as the Bundestag and Bundesrat must also still approve the legislation.

November 2025

Pay Transparency from 2026

By June 7, 2026, the EU Directive on Pay Transparency must be transposed into national law and adapted to the Pay Transparency Act, which has been in force since 2017. The goals are to prevent gender-based wage discrimination and promote salary transparency.

The current law applies to companies with 200 or more employees; companies with 500 or more employees are required to report on equal pay practices. Gender-based pay gaps are to be eliminated, and salary structures are to be analyzed.

Based on the existing regulations, courts have recognized female employees’ right to equal pay for equal or equivalent work. For example, a court awarded a higher wage to a female employee who invoked the Pay Transparency Act because the male comparison group received higher compensation. The employer had failed to sufficiently demonstrate and prove how the gender pay gap had been created. Criteria such as professional experience, length of service, and job quality were assessed and weighted to ensure compliance with the principle of equal pay.

In companies with 200 or more employees, there is a right to request information about comparable pay from a group of at least six people performing the same or equivalent work. Furthermore, companies with 500 or more employees are required to review and report on whether equal pay exists within the company. The report must be broken down by gender and include both full-time and part-time positions. The changes introduced by the EU Directive will result in an individual right to information about comparable pay in all companies, regardless of the number of employees. This information must be provided within two months of the request.

Companies with 100 or more employees are also required to submit a report on equal pay every three years, starting on June 7, 2031. For companies with 150 to 249 employees, the obligation to disclose salary information applies from 2027 onwards, and companies with 250 or more employees must comply annually from 2027. Companies with 50 or more employees are required to disclose the starting salary and its range before the application process. This is always based on the previous year’s salary. Whether national legislation requires disclosure of salary criteria is still unknown. Applicants may no longer be asked about their previous earnings.

October 2025

October 2025

Tax exemption upon reversal of a share transfer

The Federal Fiscal Court (BFH) had to decide whether the reversal of a transfer of GmbH shares between married couples retroactively eliminates the tax liability of the originally taxable transfer transaction.

A married couple, jointly assessed for income tax, agreed to a separate property regime by notarized agreement, deviating from the statutory community of accrued gains regime. The husband held a stake in a GmbH (limited liability company). To offset the accrued gains, he transferred shares in the GmbH to his wife. Based on tax advice, the couple both assumed that this transfer would be tax-free and did not declare a capital gain in their income tax return. The tax office took a different view and assessed the appropriate income tax on the transfer transaction.

The couple then entered into a notarized amendment agreement. The wife transferred the GmbH shares back to her husband as sole owner and assigned the company shares to him. They then agreed on a cash payment from the husband to his wife. However, she deferred payment to her husband. It was contractually stipulated that the spouses had assumed tax exemption in the original contract.

Both the Fiscal Court (FG) and the Federal Fiscal Court (BFH) agreed with the plaintiffs’ view and ruled that the retroactive amendment to the marriage contract should be recognized, as the spouses were able to demonstrate and prove that they had only entered into the original contract in this way because they had agreed to tax exemption. Thus, the basis of the transaction had, by way of exception, ceased to exist.

In particular, it was irrelevant whether the tax office had knowledge of the circumstances that had become the basis of the original contract.

October 2025

Waiver of compulsory portion in return for assigned compensation in installments

Gesetzliche Erben sind pflichtteilsberechtigt, wenn sie nahe Angehörige sind, z. B. Kinder und Ehepartner, Eltern kann ein Pflichtteil zustehen, wenn Erblasser keine Abkömmlinge (Kinder oder Enkel) hat.

Der Pflichtteilsverzicht ist vor allem für vermögende Erblasser mit illiquiden Vermögenswerten, wie z. B. Immobilien oder Unternehmen, ein Instrument, im Erbfall die Zerschlagung oder Veräußerung der Vermögenswerte unter den Erben bzw. Pflichtteilsberechtigten zu vermeiden. Die Gestaltung eines notariellen Vertrags mit Pflichtteilsverzicht erfolgt in der Regel durch eine angemessene Abfindung. Anderenfalls könnte er sittenwidrig sein. Eine rechtliche Beratung sollte neben der steuerlichen Beratung zuvor in Anspruch genommen werden.

Hierneben sind aber auch die erbschaft- bzw. schenkungs- und einkommensteuerlichen Folgen eines Pflichtteilsverzichts gegen Abfindung zu beachten, die je nach Gestaltung unterschiedlich sein können. An dieser Stelle soll ausschließlich eine Betrachtung der einkommensteuerlichen Seite erfolgen.

Hierzu hatte das Hessische Finanzgericht (FG) über folgenden Fall zu entscheiden: Eine Pflichtteilsberechtigte hatte zu Lebzeiten ihrer Eltern per notariellem Vertrag auf ihren künftigen Pflichtteilsanspruch verzichtet. Der zukünftige Erbe, ihr Bruder, verpflichtete sich zur Zahlung einer zinslos gestundeten Abfindung in Raten. Eine Rate wurde innerhalb eines Jahres nach Vertragsschluss fällig, die andere später. Diese Forderungen traten die Eltern an die Pflichtteilsberechtigte ab. Die Raten wurden pünktlich gezahlt.

Grundsätzlich stellt der Verzicht auf einen noch nicht entstandenen Pflichtteilsanspruch vor dem Tod des Erblassers nach der Rechtsprechung des BFH keinen einkommensteuerbaren Vorgang dar.

Eine Abfindung in Raten an eine pflichtteilsberechtigte Person ist nach der BFH-Rechtsprechung ebenfalls nicht einkommensteuerbar. Auch kann eine Ratenzahlung (zinslos) gestundet werden, allerdings nur bis zu einem Jahr. Bei zinslosen Stundungen von über einem Jahr ist in der Regel ein fiktiver Zinsertrag mit einem Zinssatz von 5,5 % durch Aufteilung der Raten in einen Kapitalanteil und einen Zinsanteil vorzunehmen. Der fiktive Zinsertrag ist zu versteuern.

Im vorliegenden Fall hat das hessische FG entschieden, dass ein Pflichtteilsverzicht gegen Abtretung einer Forderung insoweit Einkünfte aus Kapitalvermögen darstellt und nicht steuerfrei ist, als es lediglich um den Zinsanteil der zweiten Rate geht. Dies gilt auch dann, wenn die Rate in Gestalt eines Abfindungsbetrags zinsfrei gestundet wird. Der Fall sei nicht mit dem eines Verzichts auf einen noch nicht entstandenen Pflichtteilsanspruch vergleichbar.

Die Besteuerung des Zinsanteils erfolgte im zu entscheidenden Fall jedoch anstatt zum persönlichen Einkommensteuertarif mit dem in der Regel geringeren gesonderten Steuertarif. Dies ist zwar bei sich nahestehenden Personen nicht möglich, das FG war hier allerdings der Auffassung, dass „nahestehend“ nicht im Sinne eines familienrechtlichen Verwandtschaftsverhältnisses zu verstehen sei, sondern im Sinne eines absoluten Abhängigkeitsverhältnisses. Eine solche Abhängigkeit sah das FG hier nicht.

Die Revision wurde beim BFH eingelegt, eine Entscheidung steht noch aus.

October 2025

Redemption of a usufruct right in GmbH shares

The Federal Fiscal Court (BFH) had to decide the following case: A mother had transferred 49% of her GmbH shares, each with a 24.5% share, to her two daughters by gift, reserving the usufruct. She received only the profit. The daughters retained the shareholder rights, i.e., membership rights, economic opportunities, and risks.

The daughters then sold the GmbH shares in the future, and the mother subsequently relinquished the usufruct and received a redemption amount. The responsible tax office (FA) taxed this amount as income from capital assets for the mother, which the mother filed a lawsuit against after an unsuccessful objection procedure. The Fiscal Court (FG) granted the claim. The BFH agreed with the Fiscal Court’s opinion that the redemption amount for the reserved usufruct of the GmbH shares was not taxable for the mother. The beneficial ownership of the GmbH shares did not lie with the usufructuary, the mother, but with the daughters, since they received the profit. The mother, as the beneficiary, is not subject to taxation.

Anyone planning to transfer GmbH shares should seek tax advice in advance to achieve the best tax outcome.

October 2025

BFH: Presumption of access questioned

The Federal Fiscal Court (BFH) had to decide a case in which the appeal was filed one day late. The plaintiff had received the tax assessment by letter. She had been away for an extended period of work. The mailbox had been emptied by third parties, including the tax assessment, against which an objection was filed late. The date of receipt could not be verified.

The tax assessment was sent on a Friday, the 15th, and, according to the then applicable three-day service requirement, was deemed to have been served on Monday, the 18th. Under the new legal situation, it would have been the 19th. The plaintiff filed an objection on the 19th, one day late under the previous version of the law. She argued that the delivery service never delivers on Saturdays, so the delivery deadline should be extended by one day. The BFH rejected this argument because mail was delivered on at least one day within the deadline, namely Monday. Since the plaintiff could not prove that the notice was received only on the 19th, nor did she deny receipt as such (in which case the tax office would have had to prove receipt), the deadline for filing an objection was missed.

Anyone who has their mailbox emptied by a third party should always have the receipt date noted on the envelope for official mail.

October 2025

Digital data exchange starts in 2026

Starting January 1, 2026, digital data exchange will take place between private health and long-term care insurers, on the one hand, and the Federal Central Tax Office (BZSt) or the payroll accounting system, on the other. Digital transmission is intended to replace the current paper-based process; manual late reporting will then no longer be permitted.

This means that employees will be disadvantaged if data exchange is not carried out correctly, both for payroll tax deduction and income tax assessment. It makes no difference whether the employer submits the reports themselves or has them done by a service provider. It is therefore strongly recommended to train staff and service providers, both internally and externally, or to acquire the necessary knowledge to review responsibilities and interfaces.

October 2025

E-invoice: Draft of a new instruction

Before electronic invoicing (e-invoicing) became mandatory for most domestic companies in B2B transactions on January 1, 2025, the Federal Ministry of Finance (BMF) published its first application letter on October 15, 2024. The BMF sent further intended additions to the associations for comment in a draft letter on June 25, 2025. The final version of the amended or supplementary letter is to be published during the fourth quarter of 2025. The VAT Implementation Decree is to be comprehensively adapted to the statutory regulations.

Errors in the first BMF letter will be corrected in the draft. It should be noted that corrupted files sent as e-invoices will be considered a different invoice. Therefore, only an invoice that conforms to the EN 16931 format constitutes an e-invoice.

The regulations on e-invoicing for small businesses in the Federal Ministry of Finance (BMF) circular of October 15, 2024, are to be adapted to the changes under the Growth Opportunities Act. For the voluntary use of an e-invoice by a small business in formats other than those permitted, they require at least the implicit consent of the respective recipient.

According to the draft, an invoice correction of the original invoice should not be required if only the assessment basis changes, e.g., due to complaints about defects during a building inspection. However, if the scope or content of the service changes, an invoice correction should be required. For subsequent fee increases, the same invoice type should be used, as, for example, for invoice corrections.

E-invoicing must also be stored in compliance with the German Accounting Standards (GoBD). Even if only the structured part of the e-invoice is subject to the 8-year retention period, the image part must be stored in accordance with GoBD.

All contributions are compiled to the best of our knowledge. However, no liability or guarantee can be accepted for their content. Due to the partially abbreviated representations and the individual characteristics of each individual case, the explanations cannot and should not replace personal advice.