Tax Law Topics

Changes to German Tax Law and what is planned

January 2025

January 2025

Adjustment of contributions and contribution assessment limits in social insurance from 1 January 2025

From January 1, 2025, a higher contribution assessment limit (BBG) will apply to general statutory pension insurance, for the first time uniformly for the eastern and western German federal states, namely €8,050 per month. Until December 31, 2024, the BBG was €7,450 (east) and €7,550 (west). In the miners’ pension insurance, the BBG will increase from €9,300 to €9,900 per month.

The BBG is the maximum amount up to which earned income is taken into account when calculating pension insurance contributions; no contributions need to be paid above this amount. The BBG will also be increased for statutory health and long-term care insurance on January 1, 2025, from €5,175 per month to €5,512.50. This is accompanied by an increase in the so-called compulsory insurance limit from €69,300 per year to €73,800. Those who earn a higher annual income can take out private health insurance or voluntarily join the statutory health insurance scheme. The reason for the increase in the BBG is that it has to be adjusted to income trends with a time delay. This means that contributions for those with statutory insurance and their employers in the upper income bracket will increase without an increase in the contribution rates.

Contributions to statutory health and long-term care insurance will also be increased on January 1, 2025 due to a further increase in the deficit. The amount of the contribution is made up of the same general contribution rate (2024: 14.6%) and the additional contribution for each health insurance fund (average rate in 2024: 1.7%). The general contribution rate will remain at 14.6% in 2025, and the average rate of the individual additional contribution has been increased by 0.8% to 2.5% for 2025. The respective health insurance companies will decide in the second half of December how much additional contribution they will actually charge. At the time of going to press, only a few decisions had been made.

The contribution to long-term care insurance will increase by 0.2% to 3.6%. The surcharges and deductions for those without children or those employed with children will remain as before.

Contributions to statutory pension and unemployment insurance will remain unchanged in 2025 at 18.6% and 2.6% respectively. The social security contribution for artists for entrepreneurs and users, which is financed on a pay-as-you-go basis, will remain at 5% in 2025, and the contribution rate for artists and journalists will correspond to that of the German Federal Pension Insurance Fund, and the insured will only pay half the contribution rate.

The amount of the contributions to be paid exclusively by the employer for reimbursements in the event of incapacity for work, maternity and insolvency (U1 – U3) or possible changes to the amounts of the contributions were not yet available at the time of going to press.

January 2025

Changes to the small business regulation from 1 January 2025

From January 1, 2025, a special reporting procedure will apply to small businesses based in Germany at the Federal Central Tax Office (BZSt) to make use of the small business regulation in other European countries. Conversely, small businesses based in other European countries with operations in Germany submit an electronic sales tax return to the BZSt within one month of the end of the quarter.

Tax exemption applies up to a total turnover limit of €25,000 for the previous year and €100,000 for the current year. If the limit of €25,000 is exceeded in the current year, the small business regulation cannot be used in the following year. If the turnover of €100,000 is exceeded in the current year, the small business regulation no longer applies from exactly that point in the current year. The entrepreneur himself must keep an eye on the €100,000 limit throughout the year, because the tax advisor receives the documents with a delay. It is important to discuss the procedure in advance at the beginning of the year.

For new companies, the €25,000 limit represents an absolute limit in the first year. Sales exceeding this limit are subject to standard taxation. Sales made up to that point remain tax-free.

For small businesses, there are simplified invoice regulations and reporting obligations, which the tax advisor will provide detailed information about. Small businesses only need to be able to receive e-invoices. They are not obliged to send them.

January 2025

Open tax cases – changes to the Annual Tax Act 2024

The Annual Tax Act (JStG) 2024 will come into force after publication in the Federal Law Gazette, which was not the case at the time of going to press.

The law contains around 130 individual measures with various legal changes that come into force immediately after publication and can affect open issues, e.g. in tax assessments. If taxpayers also receive current amendment notices, these must be submitted to the tax advisor for review if they do not receive them directly.

Measures of the JStG that have retroactive effect on the 2023 and 2024 assessment periods are relevant for the preparation of the 2023/2024 tax returns. Selected examples of this will be reported on in the following issue.

Many of the measures will take effect from January 1, 2025 in the context of corporate and tax planning, some of which have already been prepared here (see also sections 3 – 5 in this issue). We will report later on their entry into force from January 1, 2026 or thereafter.

January 2025

Change in the threshold for monthly VAT returns

Unternehmen mit einer jährlichen Umsatzsteuerzahllast über 7.500 € mussten bis 31.12.2024 noch monatlich Umsatzsteuervoranmeldungen abgeben.

Aufgrund einer ab 1.1.2025 geltenden Änderung im Umsatzsteuergesetz durch das 4. Bürokratieentlastungsgesetz ist die Abgabe der Umsatzsteuervoranmeldung für Unternehmen mit einer Umsatzsteuerzahllast nun bis zu 9.000 € nur noch quartalsweise erforderlich. Betroffene Unternehmer sollten sich hierzu mit ihrem Steuerberater besprechen.

January 2025

Change in the average rate and the flat-rate input tax for farmers and foresters

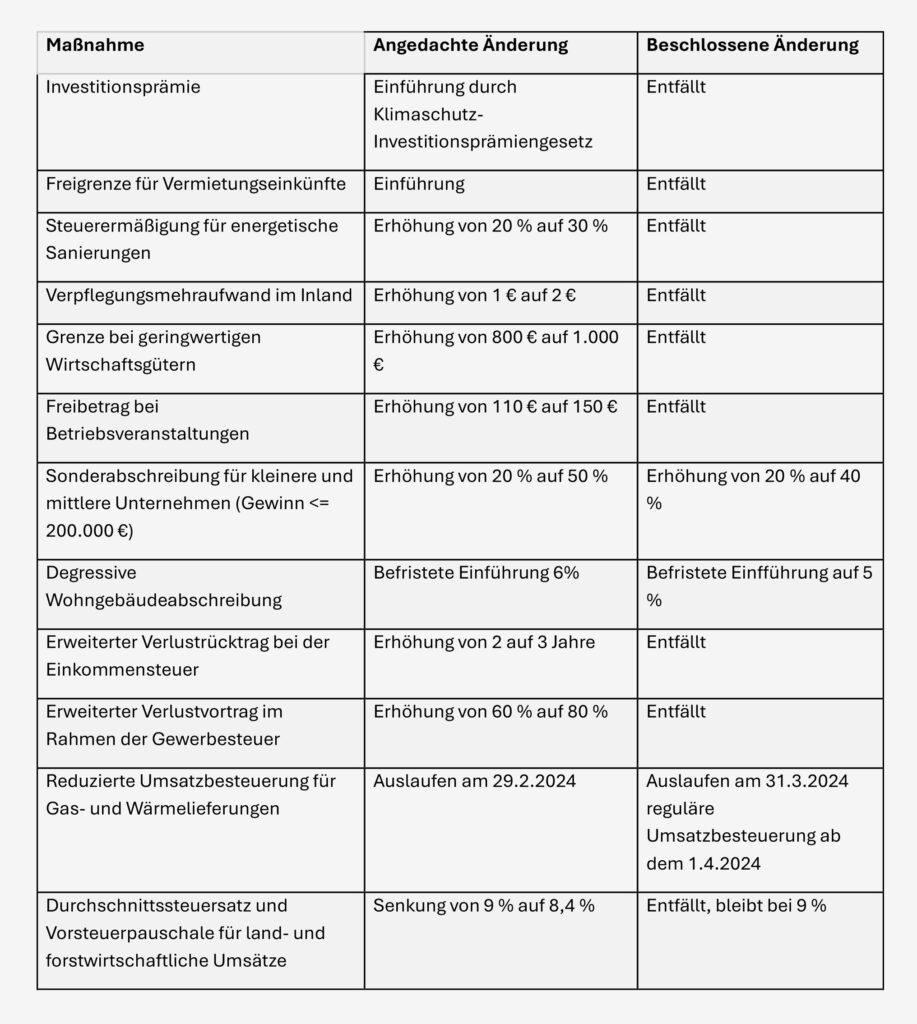

Land- und Forstwirte mit einem Gesamtumsatz von bis zu 600.000 € können im Rahmen der Umsatzbesteuerung die Durchschnittsbesteuerung / Vorsteuerpauschale nutzen, eine vereinfachte Umsatzsteuerberechnung.

Auf Waren und Dienstleistungen wird nicht Umsatzsteuer von 7 % bzw. 19 % ausgewiesen abgeführt, sondern auf den Nettoumsatz des Land- und Forstwirtes bislang pauschal 9 % aufgeschlagen. Im Gegenzug darf der Land- und Forstwirt keine Vorsteuer ziehen. Der bürokratische Aufwand ist geringer als bei der Umsatzbesteuerung nach tatsächlichen Umsätzen.

Im Rahmen des Jahressteuergesetzes 2024 wird die Vorsteuerpauschale ab Inkrafttreten für den Rest des Jahres 2024 auf 8,4 % abgesenkt, ab dem 1.1.2025 auf 7,8 % für land- und forstwirtschaftliche Umsätze weiter reduziert. Für einige land- und fortwirtschaftliche Umsätze gelten als Ausnahme Steuersätze mit 5,5 % bzw. 19 %. Hieran ändert sich nichts. Es sollte mit dem Steuerberater besprochen werden, ob die Nutzung der Durchschnittsbesteuerung noch lohnend ist oder zur Regelbesteuerung optiert werden soll, z.B. bei größeren Investitionen wie dem Kauf einer Landmaschine.

Achtung: Land- und Forstwirte, die zur Regelbesteuerung wechseln möchten, müssen innerhalb von 10 Tagen nach Ablauf eines Kalenderjahres die Optionserklärung beim Finanzamt abgeben bzw. über ihren Steuerberater abgeben

January 2025

Granting a loan with interest not at market rate is subject to gift tax

In its ruling of July 31, 2024, the Federal Finance Court (BFH) ruled that the benefit that arises from taking out a low-interest private loan concluded for an indefinite period in comparison to a bank loan at the usual market interest rate is subject to gift tax as a mixed gift.

However, if it is determined that a lower interest rate than the legally determined value of 5.5% is set for the case of taking out a bank loan, then only the difference between the cheaper bank interest rate and the contractually agreed interest rate is to be regarded as a gift.

The first-instance Finance Court of Mecklenburg-Western Pomerania correctly recognized that the granting of the loan was to be seen as a generous donation, but failed to recognize that a lower interest rate than the legally enshrined 5.5% does not have to be proven. Rather, it is sufficient to establish the possibility of taking out such a loan.

Furthermore, for open-ended loans, the annual value of the benefit of use, in this case the interest benefit, should be multiplied by the legally standardized factor. However, for a fixed loan term, this should be used as a factor. A fixed low interest rate cannot be used here.

January 2025

Retroactive increase in basic and child allowances decided for 2024

The legislature has retroactively increased the basic allowance by €180 from €11,604 to €11,784 and the child allowance by €228 from €6,384 to €6,612 for the 2024 assessment period. For employees, this is taken into account for tax purposes via the automatic wage tax deduction by the employer when the payroll or salary accounting for December 2024 is carried out. The increase in the basic allowance usually has a tax-reducing effect. For other taxpayers, it is taken into account in the tax assessment.

January 2025

E-prescription: Tax proof of medical expenses

On November 26, 2024, the Federal Ministry of Finance (BMF) announced that from the assessment period (VZ) 2024, tax deductibility as extraordinary expenses will also be possible when redeeming e-prescriptions for prescription drugs.

The prerequisite for this is proof of the inevitability of the medical costs incurred, which, according to the above-mentioned BMF letter, is sufficiently proven by the pharmacy’s receipt or the online pharmacy’s invoice in the case of redeeming an e-prescription. In the case of private health insurance, proof can alternatively be provided by the pharmacy’s cost receipt or the online pharmacy’s invoice.

The receipt or invoice must contain the name of the taxpayer, the type of service (e.g. name of the drug), the amount or co-payment amount and the type of prescription. For the 2024 assessment period, a receipt without the taxpayer’s name will not be objected to. In the case of minors or dependent children, you should speak to your tax advisor on a case-by-case basis.

December 2024

December 2024

Tax implications of the government crisis – what to look out for now

In Germany, a new Bundestag is expected to be elected on February 23, 2025, as the existing federal government no longer has a parliamentary majority following the departure of the FDP. The government will therefore probably no longer be able to pass its intended legislative proposals.

This affects all laws that have not yet been passed by the Bundestag or have only passed the first reading. It can also affect laws that the Bundesrat has not yet approved and may not want to approve with the current content due to the changed political situation.

The Bundestag passed the Annual Tax Act 2024 with amendments on October 18, 2024. This is on the Bundesrat’s agenda for approval on November 22, 2024.

The Tax Development Act will almost certainly not be further processed in its current form before the presumed new election, nor will the increase in child benefit and the increase in the tax exemption for the subsistence level.

The supplementary budget for 2024 and the federal budget for 2025 have not yet been passed by the Bundestag. Ongoing funding programs are not affected by a possible delay in the adoption of the budget, but newly planned funding for the economy, electromobility, etc. is initially on hold.

There are also currently several changes to the law on hold that should implement decisions of the Federal Finance Court or bring changes to the Growth Opportunities Act.

It is strongly recommended that you contact your trusted tax advisor before starting any new measures or restructuring in your company and clarify the current legal situation.

December 2024

Changes to the e-invoicing obligation for small businesses from January 1, 2025

The e-invoicing requirement for domestic companies will come into force on January 1, 2025. This has already been reported on several times.

According to the Growth Opportunities Act that has been passed, these obligations should also apply in full to small businesses. It is clear that small businesses must also be able to receive e-invoices from other companies from January 1, 2025.

It was planned that small businesses would have to send e-invoices from January 1, 2028. This is also stated in the letter from the Federal Ministry of Finance (BMF) dated October 15, 2024 on e-invoicing. This letter is binding on the tax authorities.

In the Annual Tax Act 2024 passed by the Bundestag on October 18, 2024, the e-invoicing requirement for small businesses with regard to sending invoices was deleted again. The Federal Council approved the law on November 22, 2024.

If you need advice, please contact your tax advisor.

December 2024

Submit tax documents for 2023 – deadline for tax returns prepared by consultants expires on June 2.6.2025

For taxpayers who have their tax returns submitted by a tax advisor, extended deadlines apply to the tax authorities. The deadline for submitting tax returns for the financial year ending in 2023 is June 2, 2025 for the tax advisor. For farmers and foresters represented by tax advisors with a different financial year, the deadline for submitting tax returns for the 2023/2024 financial year ends on October 31, 2025 or November 3, 2025, depending on the holidays within the federal states.

Documents and receipts must be available so that the tax advisor can meet the deadline. Clients should discuss this with their tax advisor.

Even if in most cases no receipts have to be submitted to the tax office with the tax returns, the so-called retention obligation still applies. According to this, the receipts must be able to be submitted to the tax office on request, so that ideally they are submitted to the tax advisor before the tax return is prepared.

December 2024

Claim flood damages for tax purposes as a landlord of real estate

Flood situations in Germany are currently and have been causing personal and economic problems in recent years when property, building and inventory are damaged. Those who do not have natural hazard insurance to cover damage suffered often have no choice but to mitigate economic damage by taking it into account for tax purposes. The respective tax authorities of the federal states have passed disaster decrees for this purpose.

While tenants and owner-occupiers of real estate can only claim economic damage as an extraordinary expense for tax purposes, taking into account the legally regulated reasonable personal contribution, landlords of real estate have the option of deducting it as advertising costs or as business expenses if it is a commercial rental. Expenses for the repair of damage to buildings and land or, for example, for reconstruction when the building structure is destroyed can be included in the tax return immediately in the year of implementation and payment of the invoice up to 70,000 euros using a special and simplified tax rule. The expenses must actually have been incurred. Alternatively, they can be spread over 2 to 5 years. If state aid or benefits from aid funds are received, corresponding reductions must be made to a maximum of €70,000 or, in the case of landlords, the state aid must be declared as income in the tax return. Above €70,000, the tax office will carry out an individual audit.

If expenses have been incurred to rebuild the destroyed building, a special depreciation allowance of up to 30% can be claimed if the damage repair is started by the end of the third year after the damage event, regardless of the amount of the expenses incurred.

Property owners affected by flood damage, whether landlords or not, should seek advice from their tax advisor on the tax rules and any special regulations.

December 2024

Tax relief for childcare costs of single parents in the shared care model

The Federal Fiscal Court (BFH) has published a fundamental decision on the tax deductibility of childcare costs in the parity alternating model. In principle, childcare costs can be deducted from tax as special expenses to a limited extent.

In the parity alternating model, the question arises as to whether both parents can each claim half of the childcare costs for a daycare center, after-school care center or childminder if they have actually shared the costs or offset them against child benefit or maintenance.

The BFH has decided that the prerequisite for tax consideration is not only that the child belongs to the household of both parents, which is the case with the parity alternating model, but that the actual transfer from the child’s own account to the account of the care facility is also required. Indirect cost coverage does not meet the requirements.

The safest way from a tax perspective is for each parent to transfer half of the care costs directly from their account to the account of the care facility. When parents reimburse each other for costs, actual transfers must be made and the underlying agreement must also be verifiable.

Irrespective of this, both parents receive the tax allowance for children as part of the more favorable assessment compared to child benefit. Only one parent receives the additional relief amount for single parents if all other requirements are met. Receipt does not depend on which parent receives the child benefit. The parents should, if possible, agree on who will claim the relief amount. If they do not make a decision, the parent who receives the child benefit will receive the relief amount. For tax simplification reasons, the Federal Fiscal Court has also considered it constitutional in the case of the equal alternating model that the relief amount is not divided between the parents.

Affected parents should seek advice from their tax advisor to clarify these questions before the start of the calendar year.

December 2024

Provision of meals or accommodation by the employer (expected values from 1 January 2025)

Employees who take advantage of meals offered to them by their employer free of charge or at a reduced price will have these meals counted as a monetary benefit within the scope of their employment relationship. This must be taxed accordingly. The non-cash benefits are expected to increase compared to the previous year. The Federal Ministry of Finance (BMF) last provided information in a letter dated December 7, 2023 about the non-cash benefits that will apply from January 1, 2024. A draft is currently available for the non-cash benefits from January 1, 2025. The non-cash benefits are then as follows (values for 2024 in brackets):

• for lunch or dinner, the value is €4.40 each (previously €4.13)

• for breakfast, €2.30 (previously €2.17)

• for full board (breakfast, lunch and dinner), the total value is €11.10

(previously €10.43)

These regulations also apply to meals that are provided or allocated to employees during business trips or when maintaining two households, if the price of the meal does not exceed €60. Otherwise, the total value of the meal represents a monetary benefit.

If the employer provides an employee with accommodation free of charge or at a reduced rate, a distinction is made between general accommodation and shared accommodation. For the use of shared accommodation, the non-cash benefit depends on how many people are occupying it. The more people occupy it, the lower the non-cash benefit. The amount of the non-cash benefit for accommodation also depends on whether an adult employee or a young person or trainee is living there.

For example, for general accommodation provided to an adult employee for individual use, a monthly non-cash benefit of €282 is used as the basis, whereas for a young person or trainee, it is only €239.70. Different values apply for the provision of accommodation; in case of doubt, the local rent applies.

Due to the lack of a majority, the final values will probably not be adopted until 2025.

December 2024

Deutschlandticket 2025

In view of the planned new elections, it is uncertain whether the Deutschlandticket will remain in its current form in 2025. One federal state has already announced that it will withdraw its funding. Up until now, a price of €58 was being considered. If the ticket remains in place in 2025, subsidies for the Deutschlandticket can be paid by the employer tax-free and free of social security contributions in addition to the wages already owed. The subsidy is limited to the amount of the employee’s expenses.

November 2024

All contributions are compiled to the best of our knowledge. However, no liability or guarantee can be accepted for their content. Due to the partially abbreviated representations and the individual characteristics of each individual case, the explanations cannot and should not replace personal advice.

November 2024

Fake tax notices circulating by post

In Lower Saxony, the police and tax offices are warning against fake tax notices that are sent to citizens by post. Fraudsters try to steal money from potential victims with letters that look deceptively real. For example, letters were sent that supposedly came from the non-existent tax office in Bad Salzdetfurth and requested payment of 762.53 euros into an account at the Sparkasse Weser-Elbe. Those affected should check the letters carefully: Are the tax number and personal data correct? Does the specified tax office exist? If in doubt, do not make any payment and contact the responsible tax office or the police. Anyone who has already paid should inform their bank immediately. For detailed information, please visit the website of the LKA Lower Saxony: Fake tax notice by post.

November 2024

Inflation compensation premium still tax-free and exempt from social security contributions until December 31, 2024

The so-called inflation compensation premium is part of the third relief package from 2022. Its introduction gives employers the opportunity to give their employees additional payments or benefits in kind up to a total of €3,000 in addition to the wages already owed. The grant must make it clear that this is the inflation compensation premium. This amount is exempt from tax and social security contributions.

However, there is no obligation for the employer to pay or grant it. The premium can also be paid in installments. The employer can choose the amount.

In the case of income-related social benefits, premium payments received are not counted towards reducing benefits, as is the case with Christmas or holiday bonuses, for example.

Even if the employee has no legal entitlement to the premium, this nevertheless means that the principle of equal treatment must be observed if it is granted. The principle of equal treatment is upheld when like things are treated equally and unequal things are treated unequally. For example, the employer is entitled to pay employees with a lower monthly salary a higher bonus than employees with a higher monthly salary.

If there is a works council in the company, there is a right of co-determination in the distribution of the inflation compensation bonus.

The preferential period runs until December 31, 2024.

Attention: On April 25, 2024, the Federal Court of Justice decided that the inflation compensation bonus represents earned income that is generally subject to seizure within the statutory limits, since the legislature has expressly not declared the inflation compensation bonus to be exempt from seizure, nor does it represent a hardship allowance and is not earmarked for a specific purpose.

November 2024

Significant fee increase planned for court register entries

The registration fees in the commercial, cooperative, company and partnership registers are to be increased by 50% due to significantly increased material and personnel costs at the registry courts.

In view of the strained budget situation of the federal states, the expenses of the registry courts are to be largely refinanced through the fee income. This is what the draft bill of the Federal Ministry of Justice (BMJ) envisages. An overview of the previous and planned fees can be found on the BMJ’s homepage.

The fee increase is to come into force on the 1st of the month following the announcement of the amendment to the regulation. Affected associations had until August 30, 2024 to comment on the draft. The Federal Council must also approve it.

Companies can therefore certainly accelerate new or amended entries that are necessary anyway in cooperation with their notary’s office.

November 2024

Partially paid transfer of real estate under scrutiny – objection advisable

The Federal Fiscal Court (BFH) has to rule on an appeal recently filed by the tax office against a ruling by the Lower Saxony Fiscal Court (FG).

The FG had decided that the partial transfer of a property by way of anticipated inheritance does not constitute a taxable private sale transaction if the property was sold for a purchase price below the historical acquisition costs. In this case, there cannot be an actual increase in value on the part of the purchaser, so taxation is not possible. Otherwise, a fictitious taxable income would be taxed.

In the court’s opinion, such a contract design is also not an ineffective circumvention transaction.

The BFH will have to clarify whether the sale of a property to a relative within 10 years of purchase for a price below the historical acquisition costs nevertheless represents a profit from a private sale transaction.

Affected taxpayers should contact their tax advisor and seek advice so that the relevant notices are kept open until the Federal Fiscal Court makes a decision.

November 2024

Fictional receipt of tax notices from 1 January 2025 now after 4 days

If authorities send administrative acts, e.g. notices, this is currently still done in the majority of cases by post with a “simple” letter, i.e. without a concrete way of tracking when the letter was received by the recipient.

For this reason, there is a legal presumption rule as to when the letter will reach the recipient. In the past, this period was 3 days. However, since the delivery time specifications were extended in summer 2024, the presumption rules for the delivery of administrative acts, including tax notices, have now also been extended from 3 to 4 days. In addition, according to the presumption rule, the announcement of a tax notice cannot be made on a Saturday, Sunday or public holiday. The innovation applies to administrative acts that are sent after December 31, 2024.

So if the tax office posts a tax notice on a Tuesday, the fourth day after delivery would be a Saturday. However, since the presumption rule does not apply on Saturdays or Sundays, the notice is only deemed to have been delivered on the following Monday. A notice posted on the Thursday before Easter is not deemed to have been delivered until the following Tuesday due to the public holiday following the Sunday.

However, the presumption rule can be undermined by the recipient and the time of receipt can thus be extended further if the recipient can prove that the notice was received later.

The presumption rule applies analogously to the electronic transmission of tax notices or administrative documents that are made available for electronic retrieval.

November 2024

Maintenance as an extraordinary expense in the tax return even if the recipient has assets?

The Federal Fiscal Court (BFH) has ruled that maintenance payments only represent an extraordinary burden to be taken into account for income tax purposes if the assets of the maintenance recipient do not exceed €15,500. The monthly maintenance payments are not to be included in the asset calculation – at least up to a certain point in time.

The defendant tax office (FA) had refused to deduct them as an extraordinary burden for the maintenance payer because the assets of the maintenance recipient, who was no longer entitled to child benefit, exceeded the protected assets by almost one month’s maintenance amount as of January 1 of the year in question, and this was the maintenance for the month of January. This had already been paid into the maintenance recipient’s account at the end of the previous year. The FA referred to the asset limit of €15,500 specified in the income tax guidelines.

The BFH made it clear in its ruling that the maintenance payment already made in advance should not be included in the assets, at least not during the year. Only in the following year can unused maintenance payments become harmful assets.

November 2024

Deduct energy-efficient renovation of your own home from your taxes

The planning and implementation of energy-efficient building renovation is not only interesting for landlords from a tax perspective, but there is also the possibility of taking advantage of tax benefits for owner-occupied residential properties.

A maximum of €40,000 per property, but no more than 20% of the expenses spread over 3 years can be deducted directly from the standard income tax as a reduction, provided that the tax burden is at this level. In the first and second year it is 7% each, up to a maximum of €14,000 each, and 6% in the third year, up to a maximum of €12,000. The maximum expenses that can be taken into account per property are therefore capped at €200,000. Measures that were started after December 31, 2019 and completed before January 1, 2030 can be taken into account.

To ensure that the expenses are not wasted in tax terms, a tax advisor should be involved in the planning of an energy-efficient renovation of the owner-occupied residential property.

The “Energy Measures Annex” must be submitted to the tax office along with the income tax return, with a separate form or data set for each eligible property over a period of 3 years. Various eligibility requirements are reviewed annually.

The deductibility is linked to a number of requirements regarding the eligibility of the properties, the types of renovation eligible for funding and technical requirements, and the formalities to be observed, such as non-cash payment, submission of an invoice, and implementation of the measures by a specialist company.

The prerequisite for tax consideration is that the building is older than 10 years, the applicant is the sole or joint owner, that the building is used exclusively for personal residential purposes, including free partial transfer to third parties for residential purposes, and that it is located in the EU or an area of the European Economic Area (EEA).

There are a number of measures that are eligible, starting with, for example, thermal insulation of walls, roofs and floors, the replacement of windows and external doors, the replacement or initial installation of summer thermal insulation, through to the renewal of the heating or ventilation system, the installation of digital systems to optimize operation and consumption, optimization of existing heating systems if they are older than 2 years, and the installation of efficient gas condensing technology under certain conditions. The examples given are not exhaustive.

On the other hand, the costs of issuing certificates from specialist companies or those authorized to issue energy certificates and the costs of planning support and supervision by a professionally qualified and approved energy consultant are only deductible to the extent of 50%.

It is particularly important that tax consideration cannot be made by direct deduction from the standard income tax if tax consideration has already been made in another way, or tax-free grants or low-interest loans, e.g. from KfW or BAFA, have been claimed.

In particular, the expenses must not have been deducted as business expenses or advertising costs, e.g. as home office expenses, special expenses or extraordinary expenses, e.g. for a handicapped-accessible conversion that also partially includes energy-saving measures.

Particular attention must be paid to ensuring that the same measure is not deducted as a household-related service or craftsman’s service with a partial amount for the wage portion of up to €1,200. In this case, the tax reduction for energy-saving renovations is completely lost and not just with the partial amount already deducted.

Your tax advisor will calculate which variant is preferable in the specific individual case.

October 2024

October 2024

The period for tax reduction after the inheritance usually begins with the death of the testator

If a deceased person leaves behind assets and one or more heirs, they must submit an inheritance tax return. Taking into account the amount and type of assets and the closeness of the relationship to the testator, the heirs have to pay more or less inheritance tax. It is possible that no inheritance tax is payable at all due to the personal allowance.

On the other hand, the heirs also have to submit income tax returns for the deceased from the past and possibly also for the future that have not yet been submitted. This may also be necessary several years after the death of the testator because, for example, heirs cannot be identified, communities of heirs are not divided up and thus any profits attributable to the testator can only be attributed as income much later. The heirs then have to pay the resulting income tax.

The law provides that heirs can, upon application, receive a reduction in income tax for the portion of inheritance tax that accrued in the assessment year of death or in the four assessment periods that follow.

But what if there are more than these five assessment periods between the death of the testator and tax-relevant transactions?

The Federal Finance Court (BFH) had to decide on this because, despite an application for a tax reduction, the tax authorities had assessed inheritance tax 6 years after the testator’s death but had not granted a tax reduction in income tax. This resulted in the heir being subject to double taxation of inheritance and income tax.

In the case to be decided, the matter had been delayed for so long because, due to difficulties in identifying the heir, the certificate of inheritance could only be issued so late that the inheritance could not be dealt with in taxable transactions until 6 years after the testator’s death.

The heir was of the opinion that the relevant time for calculating the deadline for granting the reduction was the time the tax was paid.

However, both the tax court and the Federal Fiscal Court saw this differently. The relevant start of the deadline is and remains the day of the testator’s death, regardless of whether the heirs were aware of it. The tariff reductions can be claimed in the year of death and in the following 4 years. It is therefore not important when the tax is paid or when notices are issued.

Affected heirs should definitely seek individual tax advice on this matter.

October 2024

No unlimited special expense deduction for private supplementary health insurance contributions for those with statutory health insurance

The Federal Fiscal Court (BFH) has ruled that people with statutory health insurance cannot deduct contributions to other private health or supplementary health insurance in full from their tax deductions in addition to their contributions to statutory health insurance, but only to a limited extent.

However, additional contributions generally have no effect, as contributions to statutory health and long-term care insurance already reach the maximum amount, so that a special expense deduction above this does not lead to any further reduction in income tax.

The BFH did not agree with the plaintiffs’ view that for people with statutory health insurance, taking out private supplementary health insurance is the only way to receive care equivalent to basic private health insurance, which is why full consideration of health insurance contributions is necessary for reasons of equal treatment.

The BFH, on the other hand, was of the opinion that this would involve double consideration of the necessary level of care.

In particular, since the plaintiffs were voluntarily insured under statutory health insurance, they would have been free to switch to private health insurance without double the burden if they were of the opinion that the benefits provided by the basic private health insurance were better than those provided by the statutory health insurance.

October 2024

Corona aid for the self-employed is contributory income for those voluntarily insured under statutory health insurance

The Baden-Württemberg State Social Court (LSG) has ruled in the second instance that the “Corona emergency aid” paid out to companies and self-employed persons in spring 2020 is subject to the contribution law in statutory health and long-term care insurance under social security law. An appeal was not permitted.

The subsidy increases the self-employed person’s profit and must be taken into account in the context of income tax. As a result, the subsidy increases the contribution for those with voluntary statutory health and long-term care insurance.

However, if the subsidy is reclaimed by the donor, the self-employed person’s profit can be reduced by the amount in the year of repayment.

The same applies to contributions to voluntary statutory health and long-term care insurance, because the basis for the amount of the contributions is the income tax assessment, which would have to be changed if the subsidy were reclaimed or, if not yet legally binding, kept open with the objection.

October 2024

Limiting retroactive payment of child benefit to 6 months is legal

The Federal Fiscal Court (BFH) had to deal with the question of whether child benefit for an entitled child should also be paid retroactively from the reason for its creation after the entitlement has been retroactively determined by notice.

In particular, the question had to be clarified as to whether the statutory exclusion period of 6 months for applications received by the family allowance office after July 18, 2019 is legal.

The BFH has decided that a retroactive payment of determined child benefit is legally compliant for a limited period of only 6 months. The period is calculated based on the time of application. The necessary evidence can also be provided later.

If child benefit is determined but is not (fully) paid out due to the statutory regulation, the child allowances can still be taken into account for tax purposes in the income tax return, without offsetting against the child benefit.

October 2024

Reduction of funding rates in the BAFA energy consulting programs from August 7, 2024

The Federal Office for Economic Affairs and Export Control (BAFA) has reduced the funding rates for energy consulting for residential buildings and non-residential buildings, systems and systems from 80% to 50% as of August 7, 2024.

This concerns the eligible consulting fees for energy consulting carried out by experts for single- or two-family houses, which are now still eligible for 50% or up to €650, and for residential buildings with 3 or more residential units, 50% up to €850. For homeowners’ associations, there is a one-off additional subsidy of €250 for the consultant who explains the results of the consultation at the homeowners’ meeting.

The advice can be used by owners, tenants, lessees and usufructuaries to support them in making decisions on the way to better energy efficiency for the building in question. Demand was so high that the funding rates had to be reduced in order to make do with the planned funding.

Anyone who does not make use of the BAFA funding advice can, under certain conditions, claim the costs for planning support as a tax reduction of 50% in their income tax return, even in excess of the above amounts. However, both together are not possible!

October 2024

Housing benefit will be increased on January 1, 2025

Housing benefit will be automatically adjusted to price and rent trends every two years from January 1, 2025 and will increase by an average of 15% or around €30 per month, following a major housing benefit reform in 2023. This has not only significantly expanded the circle of those entitled to housing benefit, but has also significantly increased the amount of housing benefit.

Housing benefit is a state subsidy for rent or, in the case of owner-occupied housing, a burden subsidy. In both cases, this is granted if your own income is not sufficient to cover the living expenses of yourself and any dependent family members in the same household. However, your own income must be high enough that, together with the housing benefit, it is sufficient to cover the legally defined needs. Otherwise, you must apply for citizen’s allowance.

State subsidies do not represent wage replacement benefits and therefore do not have to be declared as income in a tax return. The same applies, for example, to receiving citizen’s allowance (formerly “Hartz IV” or ALG II), strike pay or sick pay from private health insurance.

The situation is different, however, when receiving sick pay from statutory health insurance or ALG I. These represent a wage replacement benefit and are subject to the so-called progression reservation. They must therefore be declared in the income tax return.

Housing benefit only needs to be declared in the income tax return if, for example, a deduction is made for business expenses for the home office and the specific rental expenses are shown. In this case, the rental expenses must be reduced by the housing benefit received.

October 2024

Inflow of royalties for GmbH shareholder-managing directors

The principle is that royalties are taxed when they are received. These are usually received when they are paid out in cash or credited to the recipient’s bank account in a non-cash manner. However, if the royalty is due to a controlling shareholder-managing director of a GmbH, the royalty can be received fictitiously when it is due, namely by determining the company’s corresponding annual financial statements, in which the shareholder-managing director’s royalty claim is shown as a liability in the financial statements.

If the shareholder-managing director waives the royalty, it may be a hidden contribution.

However, the royalty is not due if it is not shown as a liability in the approved annual financial statements. This also applies if this procedure contradicts the principles of proper accounting. This is not important for the due date and thus the taxation of the shareholder-managing director’s royalty. This is now the view of the Federal Fiscal Court (BFH), contrary to the opinion of the tax authorities.

The Federal Fiscal Court referred a corresponding case back to the Finance Court (FG) after this determination, as no determinations had yet been made as to why the bonus had not been recorded as a liability in the annual financial statements. There may be various reasons for this, each of which could be assessed differently. The result of the second legal process at the FG must therefore be awaited.

The Federal Ministry of Finance has not yet adapted its BMF letter to the current legal view of the Federal Fiscal Court. Those affected should therefore seek tax advice.

September 2024

All contributions are compiled to the best of our knowledge. However, no liability or guarantee can be accepted for their content. Due to the partially abbreviated representations and the individual characteristics of each individual case, the explanations cannot and should not replace personal advice.

September 2024

Corona economic aid: Last deadline for final settlement ends on 30.9.2024

With the Corona economic aid, e.g. bridging, November and December aid, companies and self-employed people were supported from federal funds between June 2020 and June 2022 if they had experienced a significant drop in sales.

In order to help companies quickly during the pandemic and to secure their existence, the funds should be paid out as quickly as possible. The approval and payment of the funds was therefore mostly provisionally based on a forecast. It was planned to subsequently compare the forecast figures with the actual sales development and the fixed costs incurred. This comparison is done by submitting a so-called final statement. Both the application and the final statement are made by a “third-party auditor”, usually the tax advisor.

After the deadline for preparing and submitting the final statement had been postponed several times, it now finally expires on September 30, 2024.

It has happened that applications for Corona economic aid were either submitted via various third-party auditors, for example because the tax advisor changed between several applications, the tax advisor was no longer available in the meantime, or in the case of several companies in an affiliated company, the applications were submitted by different tax advisors for the individual companies.

The final settlement, however, must be carried out or submitted by a single third-party auditor, if necessary by changing. The new third-party auditor must apply for the change on the application platform itself. This is not the responsibility of the company or the self-employed person. However, all the necessary information and data from the documents already submitted must be made available to the tax advisor taking over.

It is also possible to change tax advisors after the final settlement has been made. However, the advisor must be informed of the billing number of the final settlement package or the customer number of the organizational profile. Otherwise, a change is not possible.

Attention: If no final accounts have been submitted on time by September 30, 2024, the responsible approval authorities are required to immediately initiate recovery measures for the full amount of the aid provided to the companies and self-employed persons.

September 2024

Reporting obligation for electronic cash registers and other basic recording systems from 1.1.2025

The Federal Ministry of Finance has now announced in several letters that the reporting requirement for electronic cash register systems with a technical security device (TSE) will begin on January 1, 2025. Reporting and transmission is carried out separately for each business location within one month of acquisition, start or end of leasing or decommissioning with an officially prescribed data set via ELSTER with the following information:

Name and tax number of the taxpayer

Type of certified technical security device (TSE)

Type, number and serial number of the electronic recording system(s) used

Date of acquisition or final decommissioning or use in another business location

For cash registers acquired before July 1, 2025, reporting must be made by July 31, 2025; for cash register systems acquired from July 1, 2025 and decommissioning, the one-month deadline applies. The same applies to taximeters and odometers with TSE. The vehicle registration number must also be reported here. Without a TSE, these may still be used until December 31, 2025. Affected companies should already compile the necessary data and obtain an overview of all systems used in their premises.

September 2024

Is property valuation in the federal model illegal? Financial authorities react with state decree

From January 1, 2025, the property tax for real estate will be levied according to a changed assessment basis, which is currently being newly determined for all properties in Germany and communicated to the property owners. The federal states have opted for different valuation models.

One of these models, the so-called “federal model”, is the subject of several legal proceedings. The Finance Court of Rhineland-Palatinate (FG) has decided to suspend enforcement in interim legal protection proceedings. The Federal Finance Court (BFH) has confirmed this decision. The decision in the main proceedings is still pending.

A suspension of enforcement will only be granted if there are serious doubts about the legality of the decision.

The FG and the BFH have doubts under ordinary law and constitutional law about the valuation rules to be applied to determine property values, in particular when the law determines the property value in a typical manner, without the legally regulated possibility of a property owner providing case-by-case evidence that his property value is 40% or more lower than the determined value.

The financial authorities of the affected federal states have responded to these provisional decisions with a joint state decree. This now stipulates that property owners are entitled to provide evidence of a lower value of the property. This will be taken into account if an appointed or certified appraiser or the appraisal committee determines this lower value or if a purchase price that is at least 40% lower is achieved in normal business transactions within one year before or after the main assessment date. The same applies to land subject to building leases.

The decrees are to be applied to all decisions that are not yet final, and also to final value updates if the deviation is greater than €15,000.

Berlin, Brandenburg, Bremen, Mecklenburg-Western Pomerania, North Rhine-Westphalia, Rhineland-Palatinate, Saarland (with deviations), Saxony (with deviations), Saxony-Anhalt, Schleswig-Holstein and Thuringia have opted for the federal model for property valuation.

In these federal states, the tax authorities should grant objections with applications for suspension of execution for an appropriate period of time without obtaining an expert opinion from the owner if the information on the value is conclusive. An expert opinion may have to be obtained later. Affected property owners should seek advice in the specific case to determine the chances of success.

Attention: It is important that an objection is raised against the basic notice (the first notice!) within one month of delivery and not against the property tax assessment notice or the notice with which the city/municipality collects the property tax.

September 2024

BFH has concerns about the restriction of loss deductions in forward transactions

Income from capital assets is subject to tax with considerable difficulties in the area of loss offsetting. A double loss offset restriction has been in force since 2021, especially for capital gains from futures transactions.

This means that such losses can only be offset against profits from other futures transactions or option premiums. Offsetting with other capital income is not possible. Loss offsetting is also only possible up to €20,000 per assessment year. Remaining losses can be carried forward to subsequent years for an unlimited period of time.

Tax is automatically deducted from domestic income from futures transactions. Losses are certified to the taxpayer by the bank; offsetting can only be claimed in the tax assessment, as can loss carryforwards.

For example, if you make a profit of €10,000 (before tax deduction) from dividends and a profit of €30,000 (before tax deduction) from a forward transaction, but a loss of €40,000 from another forward transaction, your bottom line is financially zero.

For tax purposes, it is not possible to offset the loss from the forward transaction against the profit from dividends, and the loss of €40,000 against the profit of €30,000 can only be offset to the amount of €20,000. For tax purposes, the taxpayer is therefore left with a profit from capital gains of €20,000 (€10,000 from dividends and €10,000 from forward transactions). Only an amount of €20,000 from the loss on the forward transaction can be taken into account for tax purposes in the relevant assessment year, the remaining €20,000 can only be offset against positive income from forward transactions in the future, with the risk of total loss if no more profits are made.

A married couple subject to tax did not agree with this restriction on the offsetting of losses. After an unsuccessful appeal against the income tax assessment and the rejection of the suspension of enforcement by the responsible tax office, they were given the right in interim legal protection proceedings before both the Rhineland-Palatinate Finance Court and the Federal Finance Court (BFH), and enforcement was temporarily suspended.

The BFH has also already seen constitutional concerns due to a possible violation of the principle of equal treatment if profits not economically achieved are taxed. A similar procedure is still pending to take into account losses on the sale of shares. Since the Federal Constitutional Court will probably be called upon in the end, a final decision will take several years.

Taxpayers should therefore keep open any decisions that are not yet legally binding and seek advice from their tax advisor for this purpose.

September 2024

Changes to reporting requirements for foreign currency accounts from 2025 at the latest

Investors who earn capital income receive a certificate from their banks about this income and any capital gains taxes that have already been paid. Both are also reported to the tax authorities by the banks that hold the accounts, but so far mostly only accounts held in euros.

If an investor has so-called foreign currency accounts from which capital income is earned, he was already obliged to report to the tax authorities himself in the past.

However, from 2025 at the latest, banks are obliged to report these directly to the tax authorities. A look at the tax certificate will provide information about whether your own bank has already made this report in the past.

Otherwise, investors should check whether they have independently fulfilled their own reporting obligation to the tax authorities before 2025.

If the banks start reporting from 2025, some as early as 2024, and a taxpayer with foreign currency accounts generates capital income from this, this will attract the attention of the tax authorities if the taxpayer himself has not previously declared such income.

In any case, there will be inquiries. If corresponding income then has to be declared subsequently, it is already too late, at least for a voluntary disclosure that exempts from punishment. The bank’s report already tells the tax authorities that there is capital income from foreign currency accounts and the accusation of tax evasion is on the table.

Attention: Holders of foreign currency accounts should immediately ask the bank that holds the account whether the notifications will be sent to the tax authorities in 2024. If this is the case, it is advisable to obtain all evidence of capital income from foreign currency accounts as quickly as possible and to seek advice from a tax advisor on the period, deadlines and possible voluntary disclosure before it is too late.

August 2024

August 2024

Choosing the right tax bracket and its importance

Choosing the right tax class and its actual impact often leads to uncertainty for many taxpayers. The good news first: If you have chosen a tax class that may be disadvantageous, you can correct this in most cases without negative consequences.

Wage tax classes only exist for employees, i.e. for income from employment and unlimited tax liability. In any case, people who have their place of residence or habitual abode in Germany are subject to unlimited tax liability. As a rule, habitual residence in Germany is assumed for more than half of the year. The tax authorities use the tax class to calculate the approximate tax prepayment, taking into account the flat-rate deduction amounts regulated by law. This is then deducted directly at the “source”, i.e. by the employer, by means of wage tax deduction and is shown on the wage or salary slip.

There are six tax classes in total. Unmarried people or people who are permanently separated are classified in tax class I. This also includes divorced and widowed people. The latter are only placed in tax class I from the year after the death of the partner.

Tax class II is intended for single parents with children in the household who are entitled to child benefit. No other people than the parents’ own children may live in the household, i.e. no life partner or the like. Tax class II is more advantageous from a tax perspective than tax class I, as the relief amount for single parents is taken into account directly in the tax deduction.

Tax classes III, IV and V are intended for married or civil partnership employees. If the married couple does not choose a tax class, they both receive tax class IV. The tax deduction is then the same in relation to income and, to put it simply, corresponds to tax class I for unmarried people. This combination should be chosen if the income is roughly the same. If couples with very different incomes choose this tax class combination, the tax office usually withholds too much tax, which is then refunded as part of the income tax assessment. There is also tax class IV “with factor”. Here, the income tax that is expected to be paid jointly is distributed between the spouses in proportion during the wage tax deduction process. This only happens upon request and if the factor is less than 1. Married couples can choose the tax class combination III and V. The tax deduction in tax class III is relatively lower and the tax deduction in tax class V is higher, as the double basic allowance is granted in tax class III, but not in tax class V. If one partner chooses tax class III, the other must necessarily receive tax class V. Choosing this tax class combination only makes sense if either one partner does not work as an employee or if the earnings as an employee are very different. If you choose this tax class combination, you are required to submit an income tax return. Taxpayers with very different earnings should be aware that they may have to pay additional tax when their income tax is assessed. However, there is better liquidity over the course of the year.

Tax class VI is for those who have other employment relationships subject to social insurance contributions or who are at fault for not providing the employer with the wage tax deduction details. The wage tax deduction is very high here because no flat-rate deductions or allowances are included. The compensation is usually made via the income tax assessment.

Since 2020, married couples or civil partners have been able to change their tax class several times a year. This makes sense if there is an impending shift in income and, under certain conditions, can also have a positive effect on the amount of unemployment, sickness or parental benefit. A tax advisor should be consulted here, because a change shortly before these events occurs is usually irrelevant if it is not made in good time.

Attention: When receiving sickness, unemployment or parental benefit, for example, the tax class at the time of receipt or the start of the year is generally decisive. Although these benefits are tax-free, they are subject to the so-called progression reservation and lead to a mandatory assessment. This means that the tax rate on the other taxable income is increased. This particularly applies to people who have income from employment, rental, capital or similar in a calendar year and also receive sickness, unemployment or parental benefits, but also to couples who are assessed jointly and where one of them receives benefits and the other receives taxable income.

August 2024

Allocation of services to the company – timing and documentation of the decision

In a letter dated May 17, 2024, the Federal Ministry of Finance (BMF) issued a statement on the allocation of items to business or private assets in the context of input tax deduction as a result of several decisions of the Federal Finance Court (BFH ) from 2022 and a decision of the European Court of Justice (ECJ) from 2021, as well as on the questions of the timeliness of corresponding notifications to the tax authorities and their documentation.

The ECJ had ruled that the tax authorities may refuse input tax deduction in relation to an item if the taxpayer has the right to choose whether it should be allocated to the business sector or to private assets, but the taxpayer has not declared to the tax authorities by the deadline for submitting the sales tax return which allocation he has made or at least corresponding indications are available to the tax authorities.

The Federal Fiscal Court had also decided that if objectively recognizable evidence is presented within the documentation period, no time-bound notification to the tax authorities is required and that this can also be done after the deadline has expired. A notification is therefore only required if there are no objectively recognizable signs.

The documentation must be submitted within the statutory standard deadline for submitting the sales tax return if there are no objectively recognizable signs of evidence. An extension of the deadline for submitting the tax return does not extend the documentation period. A decision made in the advance declaration procedure can be corrected by express notification until the documentation period has expired.

The Federal Finance Court has therefore now clarified that, in the case of an allocation option, contracts with VAT identification or designation in building permit documents, e.g. as an office wing, are also to be assessed as corresponding signs of evidence, even if they are only partially allocated to the company. The same applies to the company insurance of an object, purchase or sale under the company name, accounting and income tax treatment of the object. Nevertheless, for reasons of legal certainty, the tax office should also be notified in good time.

The principles of the BMF letter of May 17, 2024 are to be applied in open cases. The BMF letter can be downloaded from its homepage. The previously valid BMF letter of January 2, 2014 was repeated with the new letter, and the VAT implementation decree was also adjusted accordingly.

August 2024

Special leasing payment as a business expense

The Federal Finance Court (BFH) had to deal with the question of how leasing payments, in particular special leasing payments, are to be divided up when a vehicle is used both privately and professionally. Specifically, the question was whether special leasing payments, through which the current leasing rates can or could be reduced, should be divided up pro rata temporis over the months or should be taken into account in full in the year of payment in an income surplus calculation.

In its ruling of March 12, 2024, the BFH decided that special leasing payments for a vehicle used pro rata for business purposes should be divided up over the respective months of use, regardless of the time of payment, provided that the current leasing rates could be reduced as a result, which was the case here.

First of all, the total annual expenses including all fixed costs and depreciation must be determined, here including the pro rata special leasing payment spread over the total period of use, and then these must be divided into a business and private portion.

In the case of a car, the basis for allocation is the determination of the number of kilometers driven for business and private purposes in relation to the total distance. If this results in a business use share of less than 10%, the vehicle must be classified as private assets. According to the ruling of the Federal Fiscal Court, this is not based on the initially intended use, but on the actual use over the entire leasing period. In such a case, the costs for the vehicle cannot be claimed as business expenses, but only by way of a usage contribution. However, it should be noted that in the present case, the Federal Fiscal Court did not decide whether the special leasing payment could have been fully included in the rental and leasing income as advance business expenses on the basis of intended future use. Advice from a tax advisor should be sought on this matter.

August 2024

Extension of the tariff reduction for income from agriculture and forestry

The legislature had passed a tariff reduction for income from agriculture and forestry for a limited period until the 2022 assessment period. The extension of the tariff reduction, which is to apply retroactively from the 2023 assessment period for a limited period until the 2028 assessment period, was decided by the Bundestag on July 5, 2024. The Bundesrat still has to approve it, which was not the case at the time of going to press.

The tariff reduction is to take place in such a way that profits and losses from a 3-year period can be offset against each other, namely the assessment periods 2023 to 2025 against each other and the assessment periods 2026 to 2028. The regulation is to apply directly to farmers within the meaning of the EU regulation, and to other income from agriculture and forestry after approval by the European Commission. Income from forestry, inland fishing, pond farming and fish farming for inland fishing and pond farming are subject to approval.

The background to the regulation is the mitigation of profit fluctuations as a result of climate change or weather conditions. The Bundestag and the Bundesrat still have to approve the extension of the tariff reduction. At the time of going to press, this had not yet happened.

So far, a ruling by the Lower Saxony Finance Court of April 24, 2024 (4 K 6/24), which, in another lawsuit, found concerns about the constitutionality of the tariff reduction for agriculture and forestry and saw a violation of the principle of equal treatment, has gone relatively unnoticed. The appeal was allowed. This will be reported on here in the future.

August 2024

Is the energy price flat rate taxable? Appeal filed with the Federal Fiscal Court

With the Tax Relief Act 2022, the legislature introduced an energy price flat rate (EPP), which eligible persons received in the amount of €300. The law regulates the taxability of the benefit received. Depending on personal tax circumstances, a tax liability may arise. By law, the EPP is assigned to income from employment or, alternatively, to other income.

A large number of taxpayers are currently taking legal action against the taxation of the EPP. In one of the leading cases, the Münster Finance Court (FG) ruled on April 17, 2024 that an employee’s EPP is taxable and subject to tax on income from employment and that this is also constitutional. The court did not have to decide whether this also applies to beneficiaries who are not employees and who may be taxed as part of other income.

Because of the fundamental importance, the FG has allowed the appeal, which has been filed with the Federal Finance Court (BFH). A decision is not yet foreseeable. In comparable circumstances and with decisions that are not yet legally binding, taxpayers can file an appeal and request suspension of enforcement by referring to the BFH file number VI R 15/24. The tax advisor is the appropriate contact person to clarify the matter. Any tax savings are, however, minimal.

July 2024

Juli 2024

Tax classes III and V are to be abolished – spousal splitting is to remain

The federal government is planning to abolish tax classes III and V. The timing is uncertain. The change is to go hand in hand with an increasing degree of digitization and an agreement with the states has yet to be reached.

Married couples and registered civil partnerships currently automatically receive the tax class combination IV / IV, but can also receive the combination III / V or tax class IV with a “factor” upon request. The tax class combination IV / IV is usually chosen by couples whose incomes do not differ significantly or if wage replacement benefits such as parental allowance etc. are due. The basic allowance and the child allowances are not taken into account in tax class V, but are taken into account twice in tax class III. For employees whose income is subject to automatic wage tax deduction, this leads to a higher tax deduction in tax class V and a lower tax deduction in tax class III.

In summary, these couples have more liquidity available during the year. However, they are obliged to submit an income tax return in the following year. This can lead to a tax surcharge if there are no other major deductions.

The tax class combination III / V is to be replaced by a so-called factor method, in which the tax burden is to be determined realistically during the year, taking into account the respective earned income.

The so-called spousal splitting is also to be taken into account and not abolished, regardless of the tax class combination. With spousal splitting, the incomes of the partners are added together and the allowances to which they are entitled are taken into account twice. This prevents an allowance from being ignored if one partner has a low income. This reduces the tax rate for the partner with the higher income.

The next issue will look at aspects of choosing the right tax class.

Juli 2024

Second home tax for dual household management is only a limited deductible expense

Anyone who maintains a second home at their place of employment for professional reasons can claim the necessary additional expenses due to the dual household management required for professional reasons as business expenses in their income tax return. This includes accommodation costs, but not more than €1,000 per month or €12,000 per year, and other necessary additional expenses. The latter are fully deductible without restriction. These include, for example, furnishings and equipment. For the sake of simplicity, an amount of up to €5,000 is assumed to be necessary additional expenses. If a furnished apartment is rented, care should be taken to show the rent share for the furniture separately in the rental agreement. Otherwise, a division can be made by estimate.

In an appeal procedure (case number VI R 30/21), the Federal Finance Court (BFH) had to decide whether the second home tax levied by a city was one of the accommodation costs that are subject to limited deduction or one of the necessary additional expenses that are subject to unlimited deduction. The Munich Finance Court (FG) had ruled in the first instance that the second home tax was one of the additional expenses that are subject to unlimited deduction. In the opinion of the tax authorities, the second home tax should be included in the accommodation costs that are subject to limited deduction.

This distinction is particularly relevant for taxpayers because living space in large cities and metropolitan areas, including ancillary costs, costs slightly more than €1,000 per month and all accommodation costs above this amount are not taken into account for tax purposes.

However, in its judgment of December 13, 2023, the BFH ruled that the second home tax paid by the taxpayer is to be included in the accommodation costs that are subject to limited deduction. In its justification, the Federal Fiscal Court stated that the collection of the second home tax is directly linked to the use of the home, is based on the annual rental expenditure and therefore represents an actual expenditure for the use of the accommodation.

Juli 2024

No loss allowance in the year of the merger for the acquirer through offsetting

In its ruling of March 14, 2024 (case no. IV R 6/21), the Federal Finance Court (BFH) ruled that when a partnership merges with another partnership – this means the tax-neutral merger of two companies – the profit generated up to the transfer date in the year of the merger cannot be offset against the loss suffered by the transferring partnership up to that point. This applies in any case if the parties have chosen the end of December 31 of a year as the transfer date in their internal relationship.

Naturally, the companies involved choose a tax transfer date on which the tax liability of the transferring company ends and is transferred to the acquiring company. However, under commercial law, the existence of the transferring company only ends on the day the merger is entered in the commercial register, i.e. a day that cannot be freely chosen after the agreed transfer date.

According to the Federal Fiscal Court’s ruling, the tax bases, profit or loss, continue to be attributed to the transferring company and implemented in the corresponding notices.

Juli 2024

The grant recipient register is online

The Federal Central Tax Office (BZSt) is responsible for the newly created donation recipient register. This is a nationwide central register that includes all organizations that are authorized to issue so-called donation receipts. The data will be gradually transmitted to the BZSt by the responsible tax offices from 2024. Foreign organizations from EU or EEA countries can also be included in the register upon request. The prerequisite for inclusion is that the corporations meet the German criteria for being allowed to issue donation receipts. These are those that are recognized as non-profit organizations under the tax code.

Until now, there was no way for taxpayers to find out in advance whether intended or made donations would ultimately be eligible for the tax deduction as special expenses. For example, non-profit organizations often tried to obtain a privately organized donation seal of approval.

However, this meant that potential donors had only limited visibility as to whether the non-profit status still existed at the current time.

Using the donation recipient register, which can be accessed on the BZSt website, people willing to donate can now use various search parameters to search for non-profit organizations that meet the requirements for special tax deductions under German law. It is also possible to search by location, field of activity, etc. At a later date, it will also be possible to store bank details there.

Legally binding decisions, e.g. on the withdrawal of non-profit status and thus the end of the right to issue donation receipts, are entered in the register.

The bodies registered in the register transmit donations received online so that paper receipts no longer have to be issued. They can be used by taxpayers when filing an online tax return or are automatically stored there at a later date. Anyone who is not yet registered can still issue donation receipts in paper form.

Juli 2024

Flat-rate income tax also applies to company events in “small groups”

By judgment of March 27, 2024 (ref. VI R 5/22), the Federal Finance Court (BFH) ruled that since the change in the law from the 2015 assessment period, an employer can also assume the taxation of the benefit in kind through the flat-rate wage tax of 25% for company events that are not open to all members of a company or part of a company.

Many companies organize summer festivals or Christmas parties for their employees, for example. The company can make the costs incurred for this available as a tax-free benefit in kind up to an amount of €110 per event up to twice a year per employee. The employee then does not have to tax the benefit as wages and no social security contributions are payable.

If an employee enjoys more than two events per year or the costs for him and possibly an accompanying person exceed €110 per event, the excess amount is wages subject to income tax, for which social security contributions must also be paid.

However, the employer can exempt the employee from income tax and social security obligations by paying a flat-rate income tax of 25%. The tax advisor should be consulted on the procedure for so-called temporary workers.

In the case to be decided, the tax office was of the opinion that the employer was not entitled to flat-rate taxation because there was no company event, as the event was not accessible to all employees, but only to a select group of senior managers and board members.

In the past, according to the case law of the Federal Fiscal Court, the opportunity for all employees of a company or part of a company to participate was a prerequisite for recognition as a company event. After the legislature amended the law accordingly, but despite the established case law of the Federal Fiscal Court on this point did not explicitly include this requirement in the law, the court now assumes that since the change in the law in 2015, a company event can also exist if it is not accessible to all employees.

Juli 2024

No loss allowance in the year of the merger for the acquirer through offsetting

By judgment of March 14, 2024 (case no. IV R 6/21), the Federal Finance Court (BFH) ruled that when a partnership merges with another partnership – this means the tax-neutral merger of two companies – the profit generated up to the transfer date in the year of the merger cannot be offset against the loss suffered by the transferring partnership up to that point. This applies in any case if the parties have chosen the end of December 31 of a year as the transfer date in their internal relationship.

Naturally, the companies involved choose a tax transfer date on which the tax liability of the transferring company ends and is transferred to the acquiring company. However, under commercial law, the existence of the transferring company only ends on the day the merger is entered in the commercial register, i.e. a day that cannot be freely chosen after the agreed transfer date.

According to the Federal Fiscal Court’s ruling, the tax bases, profit or loss, continue to be attributed to the transferring company and implemented in the corresponding notices.

Juli 2024

VAT liability for online event services and online services