German VAT Refund

VAT

More than 170 countries worldwide—including all major European countries —levy a value-added tax (VAT) on goods and services. As today’s tax map shows, EU Member States’ VAT rates vary across countries, though they’re somewhat harmonized by the EU.

If you’re doing business in Germany, you need to familiarize yourself with the ins and outs of the country’s VAT system.

Understanding German VAT rates

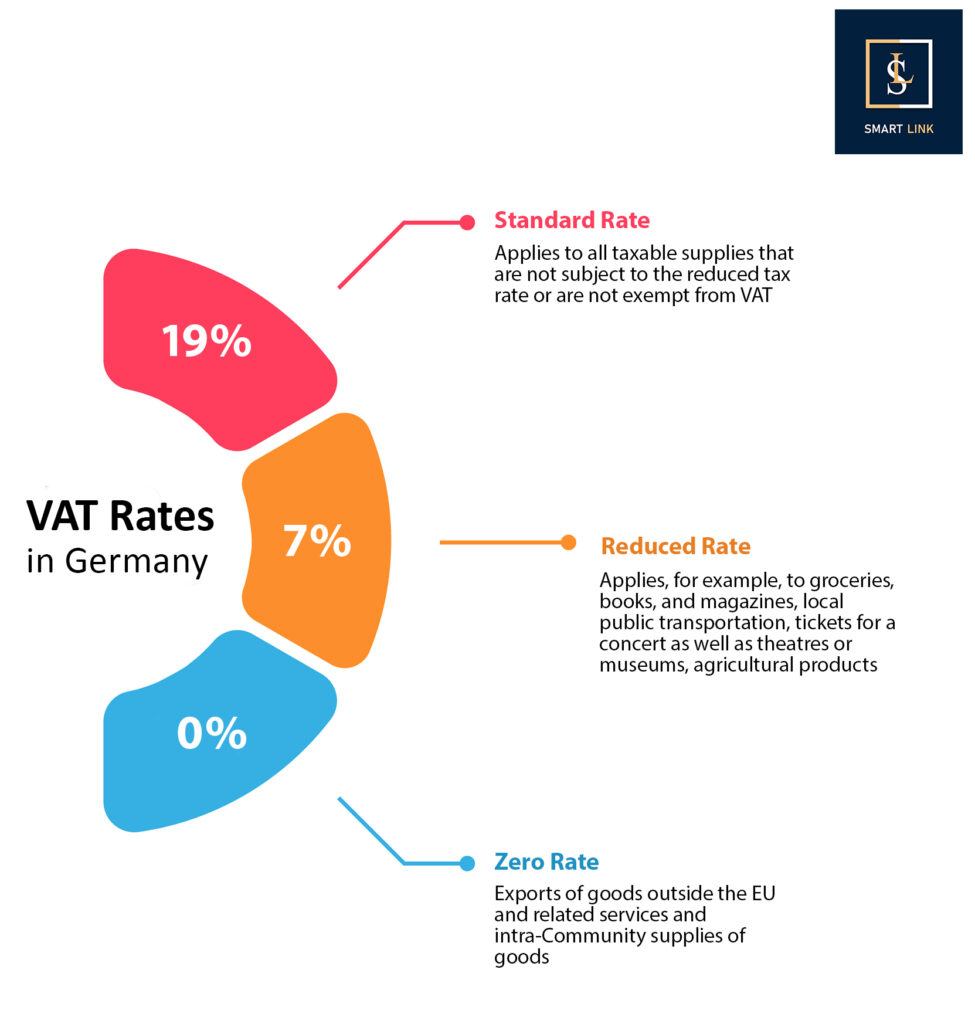

The applicable VAT rates in Germany are divided into 3 main categories: the standard rate and the reduced rate.

The standard rate, currently set at 19%, applies to most goods and services, while the reduced rate of 7% and the zero rate are applicable to specific items.

Standard VAT rate: 19%

The standard German VAT rate of 19% is applied to a vast array of taxable goods and services. From clothing and gasoline to pharmaceutical products and alcoholic beverages, the standard rate is the backbone of Germany’s VAT system.

Essentially, if a product or service does not fall under the reduced rate or an exemption, it’s subject to the standard rate of 19%.

Reduced VAT rate: 7%

In contrast to the standard value-added tax rate, the reduced VAT rate of 7% targets a specific set of goods and services. These include most food products, plants and animals, books and newspapers, works of art, and entrance fees to cultural sites. The reduced rate aims to promote the affordability and accessibility of essential items and cultural experiences.

Zero VAT rate: 0%

Certain goods and services (basic food items, medical and healthcare services, cultural services, for example) are subject to a zero-rate value-added tax of 0%. Zero-rated goods and services are treated as exempt from VAT, but the suppliers can still recover the VAT they have paid on inputs.

Registering for VAT in Germany

The registration process varies depending on the type of company, but the end goal remains the same: obtaining a German VAT number and adhering to the country’s tax regulations.

VAT Registration for local companies

Local companies in Germany are required to register for VAT if their annual turnover exceeds €22,000. To complete the German VAT registration, businesses must submit an application, registration certificate, and information regarding the directors, the form of organization of the company, the company’s activity, and expected turnover, all in compliance with German VAT law.

Upon completion of the registration process at the Federal Central Tax Office (BZSt), the company will receive a fiscal registration number, which is essential for tax filings and compliance.

VAT Registration for foreign companies

Applying for the tax number is required, along with the tax ID number, for selling various types of products such as:

- when they purchase and sell goods in the country and the goods are not removed from the country;

- when they organize live events such as conferences or art exhibitions;

- when they operate a German consignment warehouse and sell goods to German customers;

- in some cases that involve the distance sale of goods and the German registration threshold is exceeded (for example, internet retailers or Amazon traders).

Please note that these are just some examples.

Foreign companies conducting taxable transactions in Germany must also register for VAT.

Non-EU companies without a fixed establishment in Germany are usually required to appoint a fiscal representative. The fiscal representative will act on your behalf regarding VAT obligations, communications with tax authorities, and other related matters.

When do you have to register for VAT?

It is mandatory for your company to apply for VAT registration with the German tax authorities before starting your activities. Financial penalties may apply if the application for registration is submitted late.

The German VAT number

A German VAT number is commonly known as “Umsatzsteuer-Identifikationsnummer” or “USt-IdNr” and consists of the following components:

- The country code: The two-letter country code for Germany is “DE” (for Deutschland).

- The nine-digit numeric identifier: This identifier is unique to each business or individual and is assigned by the German tax authorities.

VAT compliance and filing deadlines

Once registered, businesses must adhere to the German VAT compliance rules and meet filing deadlines. This includes submitting VAT returns and adhering to monthly or quarterly deadlines.

Electronic filing of VAT returns

German VAT returns must be filed electronically using the ElsterOnline platform, the electronic filing system of the German tax authorities.

Monthly and quarterly VAT return deadlines

The deadlines for submitting VAT returns in Germany depend on the company’s net VAT due in the previous calendar year. Companies with net VAT due below €7,500 are required to submit quarterly preliminary returns, while those with net VAT due below €1,000 are only required to submit an annual return.

The deadline for doing so is the 10th day of the month following the indicated period. Staying on top of deadlines and submitting returns on time is essential for maintaining compliance and avoiding penalties.

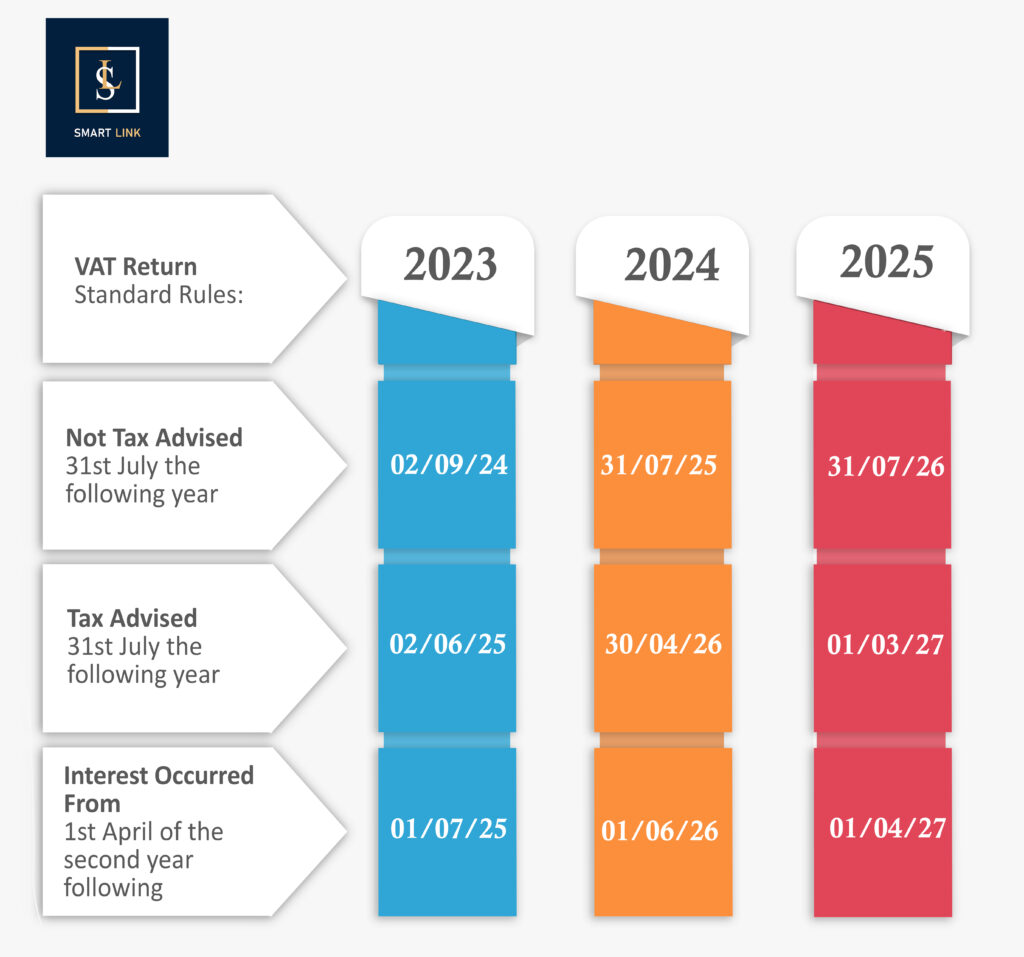

Following on from COVID-19, the German Tax Office has extended the due dates for Annual Returns due between 2020 and 2025. These dates vary depending if the company is tax-advised.

Special VAT rules for e-commerce and marketplaces

E-commerce and marketplaces are subject to special VAT rules in Germany, owing to the unique nature of their transactions and the rapidly evolving digital landscape. As a business operating, in this sector, it’s essential to understand and adhere to these rules. These include regulations on stock location, distance selling thresholds, and the One Stop Shop ( OSS).

German VAT Penalties

If there are misdeclarations or late fillings of German VAT returns, foreign companies may be subject to penalties. Late filings are subject to a charge of 10% of the VAT due, with a limit of €25,000. If the payment is delayed, there is a further charge of 1% of the VAT due per month overdue. There is a four-year statute of limitations for German VAT, except for fraud, in which case it is extended to ten years.

Germany VAT Refund For Visitors

Visitors to Germany may be able to get a refund of the German VAT tax paid on any goods bought for deportation. To get a VAT refund, you must present receipts for the goods purchased (and possibly proof of your deportation of the goods) to a Germany VAT refund station (which is often found in airports, tourist offices, or international travel hubs).